Sports Direct – Under earning, undervalued and unloved

Sep 2019 (270p)

For clients that are brave enough or open-minded enough to still be interested in our views on Sports Direct we share some new thoughts below. These are mainly in response to a patient and thoughtful read of the company’s recently published accounts and our attendance of the AGM. Hopefully most readers will by now have seen the open letter we wrote to Mike Ashley in August[1]. We also offer some context: relative to 2012, SPD revenues have doubled but its share price is the same. Today we estimate the company to be trading on an EV/EBITDA of 4x and a PE of 6x.

Blood on the high street

Baron Rothchild famously talked about the right time to invest being “when there was blood on the streets”. John Templeton embraced the same logic but with a gentler refrain (saying “be greedy when others are fearful”). Mike Ashley is taking a similarly contrarian and blood thirsty approach to the UK high street.

Price is what you pay – value is what you get

We have spent much time reading Sports Direct’s just published report and accounts – we recommend it to interested investors particularly Ashley’s 16-page CEO letter.

Our findings lend much credence to Ashley’s contrarian vigour. For example:

- Sports Direct acquired Evans Cycles for £8.7m. Included in the purchase was £7.4m of inventory.

- Sports Direct acquired House of Fraser for £90m which included £82.8m of inventory.

- Sofa.com was acquired for a pound. A cursory search of Companies House says this business had c.£1m of stock at the end of its prior financial year.

- As each of these companies was acquired out of administration (CVA – company voluntary arrangement), Sports Direct is not thus liable for the terms of the legacy lease portfolio. Crucially, SPD can walk away or renegotiate.

- These deals, and Sports Direct’s £120m sales and leaseback of the Shirebrook distribution centre follow a similar trend: Mike Ashley is going long the UK high street.

SPD sceptics and value-seekers should read the 2019 annual report – in detail.

We are very focussed on the House of Fraser deal, not least because its acquisition brought Sports Direct 4.6m sq.ft. of new city-centre store space over 54 stores. This compares to SPD’s existing UK sports retail estate of 5.6m sq.ft., an estate that still earns SPD a fairly stable £300m of gross cash flow per year – as we will show later.

HoF generated just £300m of revenues last year within SPD compared to c.£800m in each of the last two years for which it filed accounts as an independent business (2016 and 2015). House of Fraser’s £90m annual rental bill was a major factor in its demise – a factor that can be addressed resolutely by Ashley and team. More importantly HoF brings the prime located sites and space SPD’s premiumisation strategy needs. Mike Murray says this plainly:

“Earlier this year, Sports Direct’s head of elevation Michael Murray told the Sunday Times that the company planned to convert 31 stores to the Frasers format — provided it could secure three-year rent-free periods.” – Financial Times[2], August 5th, 2019 (emphasis ours)

We suspect that city by city locations are/have been renegotiated with a view to how each will fit in to supplement or replace the existing SPD store estate at a low rental cost. Additionally Ashley is busy buying up other brands (often for nearly free) to draw in future customers.

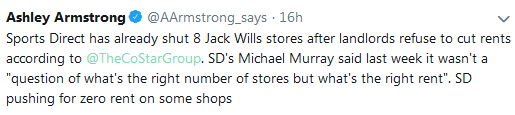

Source: Ashley Armstrong, Times Retail Journalist

Source: Ashley Armstrong, Times Retail Journalist

Other relevant points to consider:

- During the year to June 2019 HoF generated a £50m EBITDA loss within SPD, thus reducing SPD group ‘underling EBITDA’ and PBT.

- At group level, the growth in SPD’s headline group OPEX seems worrying. Until you realise that all of the OPEX growth in 2019 was all due to HoF. In fact underlying OPEX actually fell YoY in 2019. At the same time gross margins actually rose 300bps.

Method in his madness

To many the purchase of Evans/HoF, Jack Wills, BHS old stores etc looks ‘scattergun’. To us it looks opportunistic and a way to build scale. That is:

- Scale in prime high street locations

- Scale in the breadth of facia that space can be used for: USC, Flannels, Frasers

- Scale in a wide variety of brands that may draw customers and scale in its efficient distribution network of retail and online fulfilment

Our main focus is to look at the core cash generation of the existing SPD business and how that could rise were an elevation strategy be executed successfully. However the evolvement of the Fraser’s idea (with low rents and owned brands to sell in-house) has echoes of Ashley’s purchase of sportswear brand 15-20 years ago. Any hint of success in this area would catch almost all observers off guard.

Underlying Cash flow is much better than realised

Our attached model on Sports Direct shows that this company is far more profitable than it seems at first glance.

First, a word on provisions: Both your authors have ‘served their time’ analysing gritty cashflow statements both to identify companies which were over-stating earnings and less often those that might be under-earning vs their true cash flows. With such experience under our belts, we are comfortable assessing provisions. There is nothing at all wrong with provisions per se: after all, depreciation is just a provision. But let’s be clear, many provisions are highly subjective to management whims and rarely make the headlines yet they can be vital to understand underlying cashflows and thus valuing businesses.

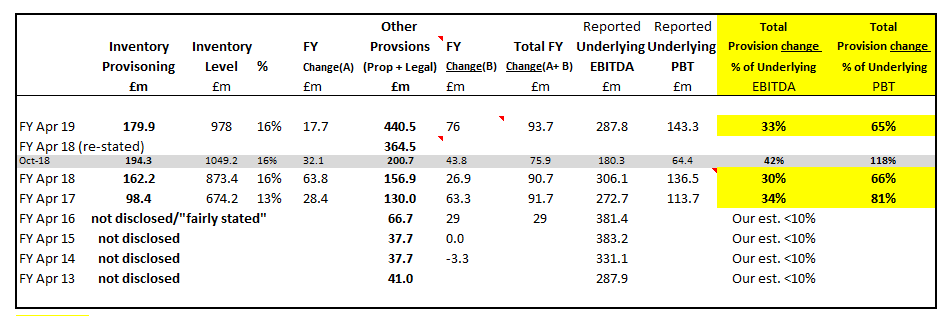

In the attached model, readers will find our work on the sizeable provisions that SPD has made in recent years. It shows that for the last three financial years SPD has been charging significant non-cash expenses to its Income Statement. These have had the effect to reduce headline profit measures such as EBIT, EBITDA and PBT. These provisions have been taken for a variety of reasons, mostly related to a more prudent assessment of inventory valuation levels and due to the cost of potentially having to exit onerous leases. Both very valid reasons, given the restructuring/repositioning of the SPD group, we might add.

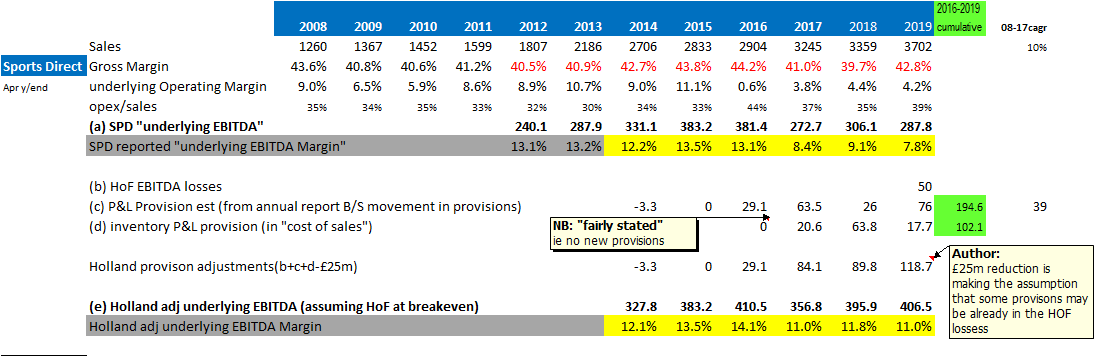

In Figure 1, we outline more detail on the provisions giving both our work to show the effect on profitability and also in our model the significant notes that describe these provisions in the recent report and accounts. (As an aside: the 2019 footnotes are unusually long and suggest that auditors requested the company to fully justify them due to their size and recent year regularity).

Our point in bringing investors’ attention to these items is NOT to suggest that they were/are wrong to be charged. This company is clearly going through significant changes and challenges and thus all the sums provided might well be need to be utilised in the future.

However due to their rising size and regularity and the fact that they are designed to be today’s estimate of future issues that may occur (with property leases exit costs or inventory valuation levels) it is extremely unlikely that they would need to keep being charged at a similar rate to future group’s accounts. AKA – All else being equal, future profitability will be higher.

To get a feel for the future earnings power of this company investors would be better to look with reference to the cash/profit generated before these items were being charged.

The table below acts as a guide as to the effect these charges have had in depressing the headline profitability this group has reported over the last 3 years.

Fig.1: Provisions materially depress SPD reported underlying profits

Source: Sports Direct Report & Accounts/Holland Advisors

For those who might argue isn’t it possible that inventory write-downs/provisions are an every-year occurrence? In response, may we point you to FY16. It is notable that in that year, Sports Direct management deemed the level of provisions as being “fairly stated” and thus did not warrant adding to. It’s not that long ago, when Sports Direct was not building provisions.

Behind the Curtain & Margins of Safety

As Ashley and his team have been allocating cash produced by the business into buying freehold properties, the asset backing for the business has increased especially when compared to the lower share price.

Interestingly, the tangible book value of SPD at April 2019 is now £1.1bn (£1.25bn – £153m goodwill) which is after the deduction of all debt (£826m) AND assuming all provisions would become an actual cash liability. The Market Cap of the company by comparison, at 270p is £1.42bn. (when we stated writing the shares were 235p!). We must of course bear in mind that c. £978m of this tangible book figure comes from the company’s inventory position, but also that there is circa £180m provision carried against it. Also that whilst Ashley might not be most investors’ favourite entrepreneur, he is not known for overpaying for assets! As such, the freehold values that sit on his balance sheet are likely realisable and prudent. In that vein, we also note the company’s depreciation policies (4-10% on freehold properties, and 20-33% on PPE). Given all of this, perhaps it is less surprising that recent stated profits and cash tax paid has been low.

A question arises then, is Ashley really the fool as he is often portrayed as in the media, or, is he a Thorndike-like ‘Outsider’; a maverick entrepreneur who instinctively ‘gets’ value, market power, cash, tax efficiency and contrary thinking – and most of all, doesn’t care what anyone thinks of him (whilst in the process making a fortune in the long-run)….?

Debt, and the cost of Sports Direct’s reinvention

When Mike Ashley first outlined the switch to a premium model (or as he interchangeably calls it ‘Elevation’, ‘next-gen’ or ‘Selfridges of Sport’!) and the move to freehold high street sites, we like other investors, assumed this would be an expensive exercise. Whilst maybe the organic rollout growth of these new stores has been slower than some would have liked, we remind readers that the sizeable HoF square footage SPD now controls does give them a window into a much improved store estate in due course. As does their opportunistic purchase of freehold strategic sites when tenants have defaulted (BHS and HoF Glasgow).

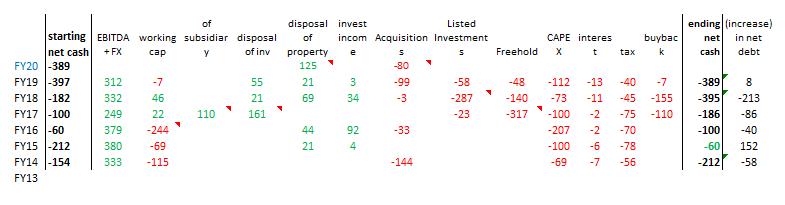

In this regard, the cost that the company has incurred to get to this level of square footage today is interesting to note i.e. it is much lower than we might have once assumed. Debt today is at a reasonable £378m (1.25x EBITDA). Our cashflow table (aka “where did the money go”) in the attached model and Appendix (table 3) is a summary that enables you to see clearly how cash was generated and spent over the past 5 years to end up at this point.

Behind the curtain

We wrote a piece on owner-controlled companies in early 2018 that also spoke specifically about SPD; the report was titles “engine overhaul”. A recent quote by Ashley might seem as if he read the report (unlikely we think).

“Sports Direct is not the future of the company. It provides the engine. These guys are putting the beautiful, shiny new car on the outside,” he says, pointing across the table to Rowley on his right and Murray and Wootton sitting to his left.. “The only thing from SD that’s saveable is the engine. It’s a very reliable sound engine, but they have to put a whole new body on it, make it fantastic, and make it relevant for the next generation. The next generation of consumer does not want the old SD way of shopping, it’s as simple as that.”. – Retail Week[3] (trade magazine), July 2019

Mike’s points are interesting when we consider the new facia the SPD group now provide customers. Elevated products may sell better under USC or Fraser facia than Sports Direct.com. Even so the brand ownership and supply chain will still be the same.

We would unabashedly recommend our note ’Engine Overhaul’ again for putting the situation at SPD today into context. The Sports Direct business model has been taken apart and it is being remodelled. During this period, it is very very hard for outsiders of the company to have almost any idea what the true earnings potential of the company might be and the real risk to different outcomes. However a better understanding what it earns today surely may help us.

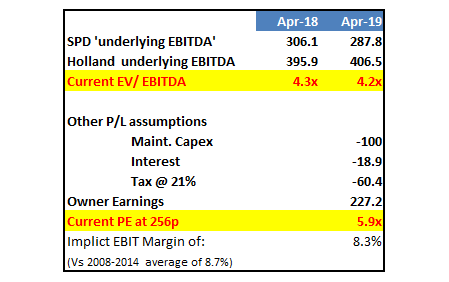

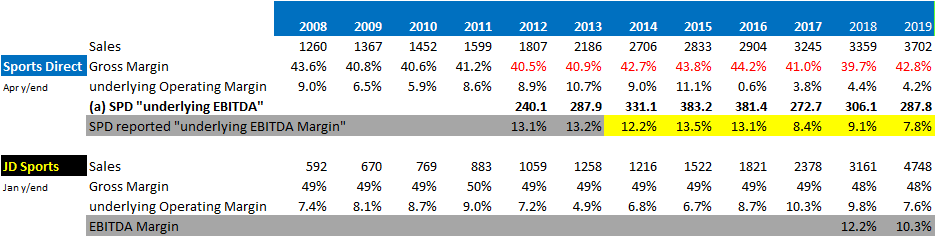

The table in the Appendix and the charts in our model that show the historical Margins of SPD and how they compare with JD Sports. We think these give a glimpse behind the curtain. They also show our best guess of what today’s Sports Direct would be earning in a steady state environment. That is, an environment where lease-termination and inventory provisions are not being charged to the P+L, where HoF losses have been curtailed (but is not assumed to make any money) and where CAPEX and tax charges are normalised.

Fig.2: Underlying cash flow under reported

Source: Holland Advisors (see Appendix for detail)

Source: Holland Advisors (see Appendix for detail)

- These figures show Sports Direct to be trading on an EV/EBITDA of 4x and a PE of 6x

- They would also suggest this company is making a return on tangible equity of c20% and an EBIT margin similar to that of its past!

- NB: current analyst forecasts have SPD making PAT of £100m for the next 3 years. Our work suggests its true PAT (owner earnings) is £227m TODAY (see Appendix)

- NB: these are not forecasts of a better outlook for SPD they are just a clean look at today’s earnings power.

How is this so? How is SPD underlying cashflow so strong?

Firstly, let’s not forget that Sports Direct, despite losing the high ground (in so-called ‘Ath-leisure wear’) to JD Sports, still operates in a sportswear market that is ultimately a duopoly. Secondly, for all its apparent failings, it remains by far the lowest price operator in the sports market.

Let’s focus on that second point – pricing. We will not re-iterate here all our past comments on SPD and its relative pricing strategy, only stating two:

- Firstly that when other companies and brands increased their pricing post the Brexit fall in Sterling, SPD did not. This meant the already sizable gap in its pricing vs. peers like JD Sports was increased further still.

- Additionally we have long believed that a future SPD business that is, by-definition, less driven by discounting would also, by-definition, be a higher margin business than the old model. Whilst we accept that the transition period to get to that end point might be complex and difficult this view we think still holds.

Yet any assessment of SPD in recent years shows lower Gross and EBIT margin levels. That is, we believe this company was/is under-earning, possibly to a significant extent. Indeed we think higher margins are logical in a now consolidated UK sportswear market. With that in mind we highlight to readers the margin section of our spreadsheet that shows gross margin in the 2019 period rose 300bp. An extract from the report and accounts helps to understand how this occurred.

“Group gross margin increased to 42.8% from 39.7%, largely due to price resetting, prior year increased inventory provisions and prior year acquisition accounting” – 2019 annual report

This is very important and in isolation might have been seen as far better news by investors were there not so many other factors affecting stated profitability and distracting investors (Belgium tax issues, loss of FD and auditor to name but a few!). For a long while now we have suggested that SPD will take its average pricing up a little and the customer would be none the wiser. Indeed Ashley’s words still ring in our ears from some years ago when he was asked how customers felt about his new product and pricing strategy he responded:

“where else are they going to go?”

Post the collapse of JJB and with JD taking the market into premium price and fashions this observation remains key.

In some ways Ashley is one of the most difficult entrepreneurs we have analysed/invested-in due to his unpredictable nature and lack of access to him and his team. That said, we have always admired his brilliant understanding of market power and when and how to use it. For years he undercut all others with his pricing. As the brands no longer want him to do that, he has pivoted knowing that by gradually moving up-market he can please them and still offers customers value vs. competitors. But in time his profits would be higher crucially because no one is pricing beneath him.

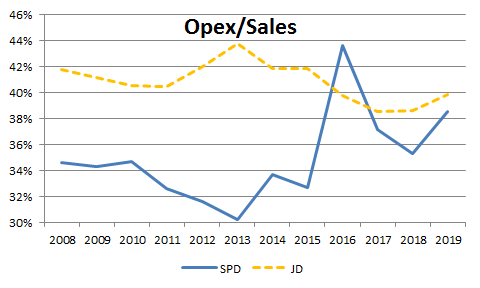

This backdrop and recent rises in gross margins suggest to us SPD has some future untapped pricing power. To put the importance of this point into context we highlight the chart below. It shows how SPD always ran a more efficient organisation than JD when purely looking at OPEX costs. Today clearly these OPEX costs are higher than SPD’s past. However as provisions and one-off HoF costs normalise, we expect the group’s reported EBIT margins will recover strongly as OPEX falls.

Fig.3: Can SPD’s operational efficiency be regained?

Source: SPD & JD Sports

Source: SPD & JD Sports

Rose-tinted glasses off. What (more) could go wrong?

Clearly this is a heading that most other commentators spend a great deal of time on. As we have stated above and hopefully as was made clear by our open (and, we hope, constructive) letter to Mike Ashley, we think there are many things his organisation could be doing better to reduce risks. We highlight two:

Risk #1: Supplier relationships and stock availability.

The company openly admitted this point in their report and accounts:

“We feel our elevation strategy is being delivered in line with the requirements highlighted to us by these brands several years ago, however we feel there remains some scepticism on their part with regards to our commitment to the full roll out of our elevation strategy…

…relationships with some key brands remain challenging where we feel we are not given full access to the product the stores deserve as quickly as we would like” – candid comments in the 2019 annual report (emphasis ours)

Furthermore, when explaining at length why the provisions are of the scale that they currently are SPD also reiterated this point:

…A number of years ago our key third party suppliers said that the Sports Direct Group had to elevate its offering away from a traditional discount model of ‘stack them high sell them low’. As has been well documented in our Annual Reports and in the media in recent years we have been on a programme of serious investment in our elevation strategy including the purchase and superior fit out of freeholds. Even though our third party brand partners by their own admission think we have done a superb job of elevating our stores, we still do not receive as quickly as we would like the premium product we feel the stores deserve. This, combined with our competition getting stronger, increases the risk of us being cut off completely by these suppliers. When we are not providing the right product at the right time…

This is a genuine and dangerous risk to this company. Whilst the Nike and Adidas’ of the world were/are prepared to do trials with SPD in their new store formats it seems the desire to open wider channels of stock supply to SPD is still not fully there. As outsiders we cannot know the exact reason for this. We can only speculate:

- Do they not trust that Ashley has changed his spots from a discounter?

- Do they just not need him with other preferred suppliers in his regions selling through well?

- Or do they not yet take SPD seriously yet as a grown-up counterpart?

The following view we did not air in in our letter to Ashley, but we should have. We think the shortcomings in the groups Finance, Management, PR, IR and other central functions might have wider ramifications for SPD than Mike and his team may realise. Local Nike executives might report up to their superiors that SPD’s in-store product profiling is indeed better, but Nike corporate head office will also see the Finance Director’s sudden departure or the lack of ability to sign an auditor as perhaps signs of unprofessionalism and delay committing to the partnership. Maybe this is understood by Ashley and his team, but the actions of the corporate centre suggest otherwise.

Also whilst we have respect for Mike Murray, would a more senior respected branded industry person/ambassador not be a good point of contact for the senior managers at Nike and Adidas? This is maybe analogous to lobbying. Few companies probably like doing it, but sometimes to get a big counterpart to move to you have to impress them from all sides.

We raised this very question at the AGM last week. The answers to which were we thought helpful. The new Chairman (ex-Nike) talked of significant efforts being made with the brands to ensure they do not judge SPD by some of the reports it gets. When we asked Ashley directly about his referencing of these risks in his CEO report (i.e. lack of quality stock availability) he said the reason for it was he did “not want to overpromise and under deliver.” Whilst we welcome this insight, this area does remain a risk for the company.

Risk #2: Management Capabilities

The more complex the operational challenges SPD faces, the less skilled hands are available to deal with them it seems.

Overall, we found the 2019 report and accounts of SPD to be encouraging as it reveals the real numbers behind the myriad of stories and distractions that take place at this company. Such as what did they pay and really get for the acquisitions they made, or how resilient is the underlying cash generation when so much else is changing.

We were far less impressed with the comments on management depth however.

“Karen Byers has been an invaluable member of the Sports Direct team for over 28 years, however as the focus of the Group moves to an elevated offering, including shop fits, this meant that Karen was no longer able to do the things she loved and was good at for so many years. Many elements at which Karen excelled now fall under the remit of third-party brands as we create the elevated stores they and our customers now demand. We wish her well for the future and consider the door to always be open if she wants to re-engage with the Group in a consultant role” – 2019 annual report

“…Mr Murray acknowledged that his arrival, unusual remuneration arrangements and closeness to Mr Ashley could cause ructions internally. It would be difficult for me as well,” he said when asked about Ms Byers. “If you’ve been part of an operating model that’s not really evolved or changed much for 30 years, it’s just got bigger . . . it’s hard for some people. Even if they want to, it’s difficult to change….But he said that elevation — steering the retailer founded by Mr Ashley away from pile-it-high outlets to a more upmarket offering — had to be about “changing every aspect of the business to modernise it”. – Financial Times, Michael Murray: the man with a mandate to take Sports Direct upmarket, Aug 9, 2019[4]

What attracts us to SPD today is the resilience of its underlying cash earnings power as we have tried to demonstrate above. However with complex tasks ahead of it such as the changing use of HoF space and the premiumisation of the company’s offering into new retail sites we think it striking that the group is losing senior talented executives staff rather than adding to them. The commentary around Ms Byers departure we find unusual and, frankly, weak.

Mike Murray’s promotion and pay must surely play a role here as maybe Ashley’s loyal lieutenants feel they are being usurped in favour of nepotism. Again, as outsiders we cannot really know. Again we will state that nothing Mike Murray has said suggests to us he is anything other than a highly capable individual, but as we outlined in our letter to Mike what this company is trying to do is highly complex and difficult. Ashley and Murray need all the help they can get especially in the areas they may be weak in. £2-5m spent on senior professionals in critical accounting, PR and branding functions twelve months ago we think could have been the difference between Nike fully stocking Sports Direct stores next summer or not. Surely that would have been worth it Mike?

A final observation we will make on skill shortages at the company is the selection of premium ranges in Flannels and Fraser’s. These we assume are also overseen by Mike Murray and his team? High priced branded fashion items is a specialist area. A look around a Flannels store shows how far this offering is from SPD’s core competency. We would feel far happier if SPD had added executive and non-executive depth in these areas. Seemingly it has not.

A word on staying rational and not fooling yourself.

“A lot of other people are trying to be brilliant and we are just trying to stay rational. And it’s a big advantage.”– Charlie Munger, 2017 Berkshire Hathaway Annual Meeting

As investors we are all aware of the pitfalls of confirmation bias – the filtering of information to suit and reinforce one’s pre-existing positions or opinions. A common trait shared by the great investors has been the ability to stay entirely rational, either to retain their position or stance in the face of what seems like new conflicting information or to change their mind based on such new information.

For us as longstanding Sports Direct and Mike Ashley supporters, in the midst of a barrage of seemingly unending and unconventional corporate chaos in the last twelve months, this is an important point to get right.

One of your authors (‘the professional worrier’) has been more resistant to accepting the Sports Direct revival story. Here’s what the worrier wrote in his personal journal back in early August upon reading the results statement:

“Significant restatements in the accounts. Not sure if the accounts can be relied upon. Not fraud, more that the accruals and m&a makes margin analysis moot. What other business has done a complete pivot on its business strategy and succeeded. Would you back M O’Leary to repeat his success if he decided to rebuild from scratch a Virgin Atlantic competitor? No – It’s a completely different strategy. – Worse, it was driven by suppliers – I.e. this business is at the behest of its suppliers – Could all of this be a red herring from the real plan – to counter cycle invest in period of high st distress to avail of huge rent concessions from landlords???? – Does this business have tech at its heart? JD seem more in tune with contemporary marketing techniques. Murray remunerated on his property investment prowess rather than his retailing” – internal Holland notes, August 2019

The point here is that just four weeks after that adlib was written, after more analysed consideration this view changed. In other words, the above initial analyst view clearly reflected emotion, not a rational analysis of the facts. Importantly, we think this is very much how the Market is approaching the Sports Direct story today – with fear, pessimism, scepticism and worse, apathy – all emotion based. By contrast, those few journalists and trade commentators[5] [6] who have had access to Sports Direct offer glimpses of an entrepreneurial culture and retail innovation.

We wrote the open letter to Mike Ashley as supporters who can see much to improve upon. Those improvements are still necessary.

Conclusion: In short – at its core, SPD is still the lowest priced operator in the market

A powerful negative narrative surrounds this company. Against that headwind, SPD generates a quarter of its Enterprise Value in gross cashflow. Additionally millions of customers rely-on Sports Direct as their go-to place for cheap sports and fashionwear. Even though these customers might not find (have found) the stores the prettiest, or staff the most helpful and even though the press and politicians have dragged the business through the mud, they still go there. In doing so they help Ashley and SPD generate £400m of gross cashflow annually. This all demonstrates that SPD has a sticky cash generative franchise and due to its starting prices vs. peers also some likely some future power.

Why do people go to SPD stores? For two reasons:

- To save money – The same reason they fly Ryanair or drink in Wetherspoons

- Because there is nowhere else to go

The risks we highlight in this report are real and do cause us some nervous reflections on this investment despite the seemingly amazing value on offer. To put them into some context however we found the following quote from the annual report of interest:

“We have continued our share buyback programme during the closed period to 26 July 2019 to continue to signal to the market our belief in the strength of the group. As our elevation strategy continues to materialise we have growing confidence in a successful future for the group in the mid to long term, thus until further notice all future buyback programmes will be up to the maximum daily volume allowed under MAR rules, currently 25%.” – 2019 Annual Report

…As the saying goes – actions speak louder than words! To sign off we will repeat a phrase we used in our letter to Ashley “To be an SPD shareholder in 2019 is to be someone who is backing Mike Ashley and taking the longer view”. Asset backing and the core business cash generation suggests there is likely little downside in these shares today. Whilst there are risks, the fact that some of these are acknowledged by the company openly gives us a little comfort.

We remain optimistic and hopeful that this group’s market position and current investment will see its true earnings power more visibly return. When it does so we think investors will reassess Ashley’s achievements more favourably than the current underlying 6x multiple of earnings today implies. Like the company itself we are very happy to be buyers of these shares.

We remain buyers of SPD.

Andrew Hollingworth & Mark Power

The Directors and employees of Holland Advisors may have a beneficial interest in some of the companies mentioned in this report via holdings in a fund that they also act as advisors to.

Appendix

Appendix 1: Adjusting for Provisions and HoF losses suggest stronger underlying profitability

Source: Holland Advisors, Sports Direct

Appendix 2: Sports Direct vs JD Sports

Source: Holland Advisors, Sports Direct

Appendix 3: Where does the cash come from and go to?

Source: Holland Advisors, Sports Direct

Disclaimer

This document does not consist of investment research as it has not been prepared in accordance with UK legal requirements designed to promote the independence of investment research. Therefore even if it contains a research recommendation it should be treated as a marketing communication and as such will be fair, clear and not misleading in line with Financial Conduct Authority rules. Holland Advisors is authorised and regulated by the Financial Conduct Authority. This presentation is intended for institutional investors and high net worth experienced investors who understand the risks involved with the investment being promoted within this document. This communication should not be distributed to anyone other than the intended recipients and should not be relied upon by retail clients (as defined by Financial Conduct Authority). This communication is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose. This communication is provided for information purposes only and should not be regarded as an offer or solicitation to buy or sell any security or other financial instrument. Any opinions cited in this communication are subject to change without notice. This communication is not a personal recommendation to you. Holland Advisors takes all reasonable care to ensure that the information is accurate and complete; however no warranty, representation, or undertaking is given that it is free from inaccuracies or omissions. This communication is based on and contains current public information, data, opinions, estimates and projections obtained from sources we believe to be reliable. Past performance is not necessarily a guide to future performance. The content of this communication may have been disclosed to the issuer(s) prior to dissemination in order to verify its factual accuracy. Investments in general involve some degree of risk therefore Prospective Investors should be aware that the value of any investment may rise and fall and you may get back less than you invested. Value and income may be adversely affected by exchange rates, interest rates and other factors. The investment discussed in this communication may not be eligible for sale in some states or countries and may not be suitable for all investors. If you are unsure about the suitability of this investment given your financial objectives, resources and risk appetite, please contact your financial advisor before taking any further action. This document is for informational purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned in it. Holland Advisors and/or its officers, directors and employees may have or take positions in securities or derivatives mentioned in this document (or in any related investment) and may from time to time dispose of any such securities (or instrument). Holland Advisors manage conflicts of interest in regard to this communication internally via their compliance procedures.

- http://www.hollandadvisors.co.uk/cms/resources/hollandadvisors-open-letter-to-spd-final-copy-26919.pdf ↑

- https://www.ft.com/content/456ed954-b79e-11e9-96bd-8e884d3ea203 ↑

- https://www.retail-week.com/sports-and-leisure/analysis-can-sports-direct-woo-next-generation-of-shoppers/7032533.article?authent=1 ↑

- https://www.ft.com/content/3bd16468-ba9e-11e9-8a88-aa6628ac896c ↑

- https://www.telegraph.co.uk/business/2019/04/14/godfather-sports-direct-inside-world-mike-ashley/ ↑

- https://www.retail-week.com/sports-and-leisure/analysis-can-sports-direct-woo-next-generation-of-shoppers/7032533.article?authent=1 ↑