Nubank – A snowball at the top of a long-wet hill

June 2024 ($11.7)

We spent some time last week thinking hard again about Nubank. We reflect further on a business we think has the potential to be very big and very important in the global banking system. We are loathe to make the Amazon comparison, but there is a scale of large industry disruption and customer centricity occurring here that suggests using such a lens is appropriate. What is also interesting is that, with a company growing very fast (c.25% of Brazilians have a Nubank as their primary account) changes in the company’s financial model are happening quickly.

7 Powers comes to life

Available on request, we have the company’s most recent investor call transcript, with our annotations. Investors with good mental models in their head we hope quickly will find much to like:

- This is a company with super-low unit-costs (c.80% below mainstream banks it estimates)

- It is hugely customer centric, i.e. trying to offer more competitive loans and deposit pricing whenever it can

- It is also very aware of its disrupter status and using it powerfully to:

a) make a noise about its brand and new products, which customers love

b) crucially to pass some of its operating efficiencies on to customers

- It is a fully capitalised bank and importantly seen as such by customers

The actions of its now 100m account holders suggest what Nu is doing is powerfully resonating. These 100m people have decided they like the competitive interest rate on a Nu credit card, or the extra money they can earn in a Nu Mexican deposit account (the 15% interest rate on offer is roughly 3x the rate other Mexican banks pay today). Crucially, 100m people have decided also to trust Nu with their money.

Reading the Nu Holdings annual report or an investor call is a little like watching Hamilton Helmer’s, 7 Powers book spring into life. The company has for 10 years (in Brazil) and for the last two years in Mexico powerfully used its upstart, counter positioning traits. This makes a noise and gets it noticed, but already this is morphing into scale economics, i.e. re-investing its unit-cost advantage to drive a bigger wedge between it and the sleepy banking incumbents.

Pattern recognition

We have had quite a few experiences of this challenger situation now in our careers and have learnt much from each of them. Often the picture is clearer nearer the end of the journey, but with Nubank currently still only powerful in one country we think we are far nearer its beginning. Great examples of counter-positioning businesses that became industry leaders include Netflix and Ryanair. We know both well and saw them real time morph from scrappy disrupters to unit cost/scale economy leaders. We often describe our job as largely pattern recognition; Nu Holdings we think, is a wonderful example of just that.

Here is what we said about counter-positioning, and how market incumbents react to it, in our Netflix piece. We think it highly relevant to where Nubank finds itself today vs its LATAM (and global) banking peers.

Counter-positioning

Sometimes it is hard to remember where you first heard something. We had read about counter-positioning before reading 7 Powers, but the book’s work on it we thought useful. We have certainly seen a great deal of real life counter-positioning via the challenger businesses we follow in Ryanair, JDW, Amazon, Schwab etc. 7 Powers articulates well the common traits that these businesses often display and how they impact incumbent players. Helmer brilliantly refers to the five stages of how incumbents react to counter-positioning. They are listed below:

- Denial

- Ridicule

- Fear

- Anger

- Capitulation (frequently too late) Source: 7 Powers, Hamilton Helmer

These are excellent and so true. Your author as an ex-airline analyst saw these close at hand when British Airways or Lufthansa was often asked about Ryanair in its early days. Denial and Ridicule were common. With Ryan’s intra-EU market share now at 16%, such companies are at the capitulation stage! Whilst we did not hear Blockbuster answer questions about early-stage Netflix, we can only imagine their replies were similar. Denial, Ridicule, then in their case bankruptcy.

Power Progression

The second area of Helmer’s work we think appropriate to highlight for Netflix is what he describes as ‘power progression’. This is his way of thinking how a Sustainable Competitive Advantage (SCA) is being developed. Holland’s approach has been to look for SCA of some form and also the presence of owner managers. Helmer links the two. For many years now we have watched great owner managers innovate and pivot businesses. Helmer rightly describes “Innovation as the first step to gaining some sort of power.”

Whilst this is not rocket-science it is a useful mental tool as we see the best owner manager’s change and adapt to new market positions. What they of course are looking for is a SCA in the future environment. We have now seen more than a few owner managers make such transitions. We have also seen Mr Market often terrified of the potential consequences during such a period of flux. (Next moving online, Facebook’s Meta/AI investment, Frasers stopping discounting++). Source: Holland Advisors: Netflix – The Discovery Channel, April 2023

A Snowball…

Nu Holding’s CEO David Velez comes from this culture (ex-Sequoia) so he knows the theory we are outlining above well we suspect. Whilst this is useful, what is more powerful to our conviction on Nu is where the business now finds itself. As per the Peter Lynch quote, repeated later, an investors job in such a situation is not to re-invent the wheel.

Instead, it is to assess whether the business in front of them is powerful and if so, to then think logically about what might happen next in its rollout. To be considered a “Snowball” in investment terms you need to possess a few traits that make the superiority of your business model over peers self-evident. Not exclusively these traits will likely include:

- Lowest unit cost,

- Differentiated product,

- High customer centricity,

- A financial model that affords growth (i.e. good ROIC)

- A visionary owner manager that knows what levers to pull

More succinctly put you need to be a horse (business model) of an exceptional standard who is being ridden by a great jockey (manager).

The long-wet hill

No matter how good the horse and jockey, what will affect your ability to grow (i.e. how fast for how long) however will be the length and gradient of the downhill of wet snow in front of you. Here is where our blood starts to pump a little quicker on Nu Holdings. Nu’s customer offering is better than all global banking peers, but cheaper to run and creates a higher ROIC as a result.

We think the Nu Holdings model is powerful and a counter positioning upstart who has already morphed into a scale economy shared model that customers love. Crucially however its competitors (globally) are asleep at the wheel. Even if they were to wake up, we are not sure what they could do to combat the threat that Nu is bringing to their door? This threat is only today being experienced by banks in Brazil and Mexico, but this mouse trap travels. Of that we are sure of – we think Mr Velez is too!

By way of an example, the Q1 Nu investor call transcript is interesting in its description of the Mexican banking market. Nu CEO David Velez explains that Mexican banking profits are largely made up of deposit spreads. I.e. the banks have been paying deposit holders 4-5% vs a 12% central bank rate, thus making almost risk-free returns. It is perhaps not odd therefore that when Nubank offers 15% to deposit account holders it gains 1-2% share of the entire deposit market in 24 months (and 6% credit card market share).

Mexican banks like all others trying to compete with Nu have dual cost bases (online and in branch) and thus need fat product margins to cover them. This means they cannot hope of competing with Nubank in terms of the interest rates offered. Deposit capital is flocking to Nubank and it is highly logical that more will follow as such a better offer is being made to the customer. Once the Mexican banks realise the scale of the existential problem facing them, they might try to cut costs to make ends meet. Likely this will mean closing branches, thus giving customers an even worse service, arguably creating a spiral with diseconomies of scale. Low headline PE’s will likely make such banks dangerous value traps. If you want to know where such a journey leads, read Nick Sleep below.

We do not live close to either Brazil or Mexico, but we suspect the incumbent banks are somewhere on that five-stage process of denial to capitulation we outlined above. We do not envy them.

Mexican bank deposit greedy profits are not replicated across the world, nor is the terrible service offered by Brazilian banks when Nubank started up. That said global banking is not an industry that has served customers well and it has been slow to change. Crucially the dual cost disadvantaged structure (online and in branch) is replicated worldwide. Additionally, no bank we are aware of has used the scale economy shared model to give customers great deposits rates say, as Nu is doing in Mexico. (The only example we can think of is JPM that sometimes uses its scale to muscle into new areas – all you can eat global research for $10k comes to mind!).

With a super low unit-cost structure and a desire to share that with customers we think this business model can travel – fast. Today it may be likely to grow further in LATAM, but why would it not come to Europe? Spain and Portugal would be our first bets. Nu’s ex-IR Director recently speculated they will target Spanish and Portuguese speakers living in US. EU/US regulators would surely welcome this deflationary force that is good for the customer. This all suggests to us Nubank might have a long-wet hill of snow in front of it. Even without such geographic expansion the company could be 8-10x its current asset (and profit) size just from its Brazil and Mexico operation’s maturing.

The future of banking..?

We wonder if a part of the Nubank investment story that is missed is the importance of its acceptance as a bank. I.e. in customers (and regulators) eyes it is not a payment platform or an FX provider, it is a fully-fledged bank with all the capital and reputational requirements for safe money that go with such a badge. An important truth is that customers think about banks very differently from how they think about money transfer platforms. That Nu’s customers compare it directly with mainstream banking peers, i.e. those that also have capital, and long-standing trusted brands is crucial.

We add to this the fact that such customers rate Nu’s service far more highly (via very high NPS scores) than they do competitors. This is despite these competitors spending 5x as much in cost terms as Nu! The longer-term implication of that statement we think all need to carefully consider.

The net result of this is a better product for the customer, and a more efficiently run bank that is much more profitable for shareholders (Brazil ROE >40%). This to us is analogous to what happened with the likes of Amazon, yes; but also say Spotify. Simply put this just looks a better banking mouse trap than the one almost all westerners are using today.

Clearly for much wider extrapolation of this model into USA and Europe, Nu needs to keep performing as it is today/become a business model others want to copy and fear. However, if it can do so, it might mean existing banking structures/entities are potentially as broken today as High Street retail was 15 years ago.

In the Appendix of this note is Nick Sleep’s discussion of Amazon vs the High Street retail offer in c.2006. Its essence was just to ask, ‘why can’t this superior business model one day have a very big market share..?’ The rest, as they say, is history! A shorter extract is shown below:

It seems to us that the basic building block of internet retailing, its skeletal structure, is far more robust, scalable and cheaper than the high street equivalent. In other words, its power law is very high, and implies that businesses with the simplicity of operation as say, Amazon.com, have a shot at being far bigger, quicker and more profitable than their high street equivalents. Nomad has an investment in Amazon for more reasons than the firm’s simplicity of operations. But when this basic building block is combined with the scale efficiencies shared model (which increases the moat as the firm grows), customer centric orientation of the firm’s founder, as well as his healthy disdain for Wall Street, this combination makes us think that we may have a mouse that can turn into an elephant. To those who argue Amazon is large already we ask two questions: what do you think e-commerce will be as a proportion of US retailing in ten-years’ time, and what do you think it was last year? Write both numbers down and turn to the end of this letter*** for the answer to the second question… (The answer was 2.6%). Extract from Nomad Investor letter 2006. Source Igy Foundation website

Sleep and his business partner Qais Zakaria dared to ask how big internet retailing could be and what that might mean for the future scale of Amazon? All we are doing here in 2024 is asking the exact same question of the online banking sector and Nu Holdings. How big could they be?

Some might regard the idea of forecasting Amazon, Ryanair or Netflix dominance 10-20 years’ ago as guesswork. We accept such forecasting is very hard, but we think there are moments when it looks a little easier. That is all Peter Lynch below is encouraging us to do. It is what we are trying to do as we balance our assessment of Nu’s seemingly powerful business model vs the existing banking industry that we assess Nu as so superior to. The actions of 100m customers so far suggests this is more than just a pipe dream.

“I don’t think that with great stocks you need a super-computer or an advanced Sun microsystems to figure out the math.”

Take the example of a company I missed: Wal-Mart. You could have bought Wal-Mart ten years after it went public. Let’s say you’re a very cautious person. You wait. Now ten years after it went public, it was a twenty-year-old company. This was not a start-up. So it’s now ten years after the public offering. You could have bought Wal-Mart and made 30 times your money.

The reason you could have done that is that ten years after it went public, it was only in 15% of the United States. And they hadn’t even saturated that 15%. So you could say to yourself, now what kind of intelligence does this take? This company has minimal costs, they’re efficient, everybody who competes with them says they’re great, the products are terrific, the service is terrific, the balance sheet is fine, and they’re self-funding. So you say to yourself, why can’t they go to 17%? Why can’t they go to 21%? Let’s take a huge leap of faith: why can’t they go to 23%? All they did for the next two decades was roll it out. They didn’t change it. I only wish they had started out in Connecticut instead of Arkansas. Source: Peter Lynch interview 2002

A powerful self-financing model

If the maths around Nubank’s business model were merely better than existing banks (say it looked set to make a 20% ROEs, by offering far more competitive products), then we would like/respect it as a business with growth potential. Arguably this is the model of companies like Costco, JDW or Ryanair. Such companies Returns on Capital are good, but not very high. Their ROE/ROIC’s of 15-25% are arrived at via high asset-turns, rather than high mark-ups. Such models have however enabled them to grow solidly by re-investing much of their profits for long periods. In turn more consumers turn up for their services.

What is exciting about Nu Holdings as an investment is that the company looks set to earn an ROE of c.40% or more we think. Doing so in a sector known for its capital intensity. Such outputs will create large sums for the company to re-invest into more industry growth at a potentially similarly high ROIC rate. In March we wrote on the subject of supernatural compounders and the traits we look for in such businesses (Holland Views : In search of Nirvana. March 2024). The more time we spend on Nubank, the more we think it one such company.

At the same time the regulated and capital-intensive nature of the banking sector means other new entrants coming behind Nu will not find catching up at all easy. This suggests to us the Nu snowball could surf down the hill at a fast rate, and even nimble competitors might wallow in its wake. (Too many metaphors? Probably!).

“In the first quarter of the year, Nu Holdings achieved an adjusted net income of US$443 million, reflecting an adjusted annualized return on equity of 27%. We believe that this performance surpasses that of most peers in the region, despite maintaining a considerable excess capital of US$2.4 billion at the holding level and with two subsidiaries in Mexico and Colombia that are still operating with negative profitability. If one were to look at our operations in Brazil alone, our return on equity remained well above 40%.” David Velez, Nu Bank CEO Q1 Analyst call 2024

It is interesting to us that Nu started in Brazil and Mexico, where competition is weak. Sam Walton of Wal-Mart built his scale vs weaker competition also.

Price is what you pay, value is what you get

Our Ryanair and Netflix learnings lead us to admire and believe in what Nubank might achieve as a disruptor that then uses its scale powerfully. Our Amazon experience maybe informs the price we should pay for such a business or at least how we should assess its valuation. Your author was for too many years, too quick to dismiss Amazon as an investment due to its high headline valuation. Only with more work and a little luck did the opportunity present itself in 2022 for him to right that wrong (Holland Advisors: Amazon – The one that got away, or did it? May 2022). Holland’s multi-year Amazon mistake was not to think far enough out to see the scale of compounding that would most likely be achieved. Particularly when the group’s high ROIC was constantly reinvested. Also, when Amazon’s near-in investment for long term growth was better considered. In that vein Nu Holdings recently disclosed that c. 40% of operational staff are working on products not part of the company’s current offering!

With this in mind there are a few ways to consider Nu Holding’s valuation today we suggest. The first is just to believe, as we do that the group can find plenty of opportunities to invest all its generated capital in the underserved banking sector globally over the next 10+ years. Simply put, if the company achieves an ROE of 30% and redeploys all that capital internally for a similar IRR, then profits/intrinsic value will grow annually at that rate, i.e. c.30%. We suspect readers would happily pay 30x earnings for such an entity. Indeed, were its PE to fall to 20x in year 10 investors IRR’s would still be c. 25%.

Underearning today

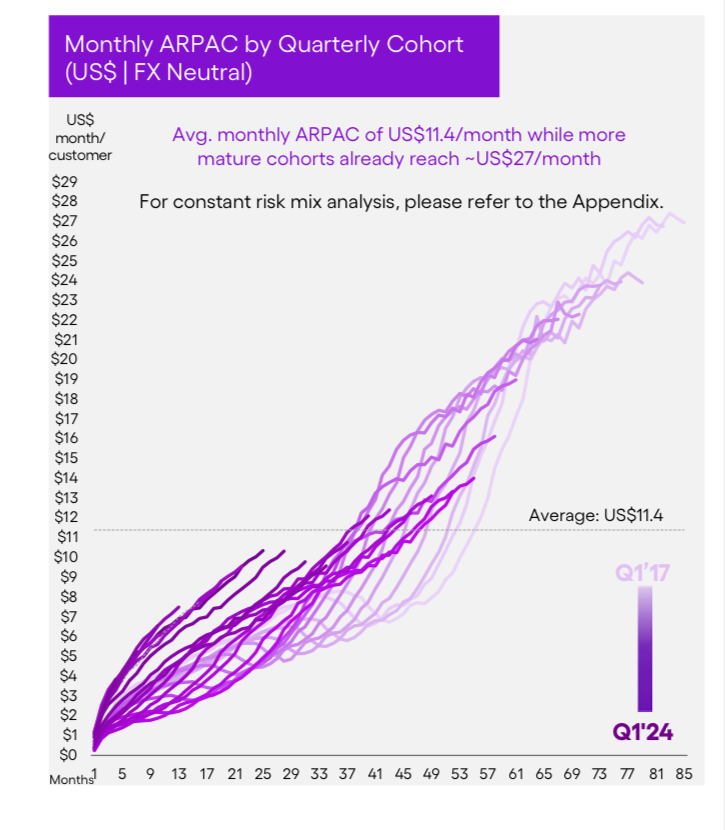

However, we also think it right to adjust Nu Holding’s current earnings as they represent a low level of maturity for existing customer spending. When we wrote on Nubank in January the company’s monthly revenue per user (ARPAC) was $10.5, having been c.$8 only 12 months previously. In just a single quarter this ARPAC has risen to $11.4.

Charts in the company presentation pack (see below) clearly show how such ARPAC trends higher the longer customers have been with the company. Crucially this is happening without significant further investment (i.e. this is just existing customers maturing with greater usage of existing products through time). Long tenanted customers have ARPAC’s of c.$27. With the company having a very low, and stable unit cost base, natural maturity improvements in ARPAC would have a huge effect on Nu’s profitability due to powerful operational gearing.

Fig.1 Nubank monthly ARPAC by year of customer joining

Source: Nubank Q1 24 Results

Source: Nubank Q1 24 Results

The adjustment we made for this in January was to assume a $15 ARPAC. Making the same adjustment now to the group’s Q1 figured just reported is instructive

- Q1 2024 Net income/annualised = $442m X4 =$1,768m

- Q1 2024 annualised ROE = 27% (c.$1,768m/$6,600m)

- Q1 2024 revenue $2,735 = $912m per month. Annualised = $10,940

- $912m/average active customers of 80.3m = ARPAC $11.4

If ARPAC adjusted to $15, then Holland underlying earnings power might evolve as follows:

- Average active customers of 80.3m x $15 = $1,204m monthly revenue

- New Q1 2024 annualised revenue of $14,448

- Implied extra marginal revenue of $3.5bn

- Despite low/stable unit costs we assume only 60% flow through to PBT + 30% tax

- Incremental revenue at $3.5bn x 60% = $2.1bn extra PBT

- After 30% tax = $1.47bn uplift in net income

- New Q1 24 annualised net income = $1,768m + $1,470m = $3,238m

- ROE = 49% ($3,238m/$6,600m)

- Look through PE = 17x ($56bn/$3,328)

NB: This ROE of 49% matches with company guidance of Brazilian ROE >40%. Also, with the scale of investment it alludes to making in new products and services.

Bumps in the road

Nubank is different to the ‘fin-techs’ that have come before. The main reason is that it is a bank. It is regulated like a bank, has the capital of a bank and is crucially trusted by consumers with their savings, like a bank. Yes, this is because of the bank’s capital base and Brazilian license (it is still waiting for one in Mexico) but also because Nubank accepts savings and offers loans, like a bank.

Reputationally this looks to be a good thing with the company now widely known and trusted in its chosen markets. That said expanding into loan products quickly or lending to the under-banked is no easy task. Whilst the company claims it is building proprietary knowledge to help its lending decisions other ambitious companies who tried to grow fast in finance have made similar predictions in the past. Thus far the company has seemingly had good lending outcomes, whilst balancing these against its market share growth ambitions. We are not blind to the idea that such good credit outcomes will always be the case. Indeed, with likely plans to expand in more countries, for the company not to have some sort of credit hiccup would be surprising. The right question on this for investors: Is the danger of such an event enough to dampen the otherwise powerful compounding on offer? Alternatively, we should remind ourselves that the last ten years in Brazil have hardy been smooth sailing economically, i.e. this business has been built in a tricky lending environment. The above comments come under the risk category that all banks possess, ‘credit risk’. The reality that we fully accept is that history proves this risk often lands more at the door of newer lending institutions who have a greater focus on growth. Our eyes are open.

A separate risk for Nubank must also be considered, that of political risk. Wal-Mart and Amazon grew the scale of their businesses in their home US market, Nubank is starting in Brazil and Mexico. Whilst these markets have weaker banking competitors such regions do not come without real political risk. Recent elections in these countries and political attitudes towards free markets and central bank independence are evidence of that fact.

When considering competitive risk, we are looking for Nubank potential global peers, and in truth not finding many. We find disruptive fintech’s (Monza, Revolt, Sony Bank, Rakuten, N26) almost all of which however are assets light money transfer businesses. They offer better value services than mainstream banks, thus are well set to keep stealing incumbent’s FX and related revenues. As yet, however we have yet to find another sizable, fully regulated truly digital bank, i.e. one taking deposits and making loans. We are open to ideas on this point from readers. Are there other global companies that might more closely compare with what Nubank that we should be looking at?

In summary

We love disrupter business with super low unit-costs. We love them even more when they have high ROIC/ROE business models, thus can self-fund their growth. When such a company also has a long runway of growth ahead and is led by a passionate, visionary owner manager we think there is good reason for excitement. As we asserted in January, maybe Nubank will prove itself to be a “Supernatural Compounder”. We take a moment just to remind you of a little maths from that note; a ten year 30% compounder is worth 14x its starting capital value.

The credit and political risks at Nubank are clear and not to be easily dismissed. For Nubank, like Amazon fifteen years ago, the scale of the opportunity in front of it is potentially enormous. To deliver on such opportunity will require tackling difficult challenges (just like Amazon building a last mile network or its AWS division). Also, maybe just a touch of luck (no political disasters in Nu’s core countries in next 5y). The reality is that bumps in the road are an inevitable part of such a company’s future expansion. If the core Brazilian division can be grown through ARPU expansion as the company suggests it will become an enormous cash cow many times its current size. That (at =/>40% ROE’s) will both fund expansion and allow a few mistakes elsewhere along the way.

With kind regards

Andrew Hollingworth

The Directors and employees of Holland Advisors may have a beneficial interest in some of the companies mentioned in this report via holdings in a fund that they also act as managers to.

Appendix

Extract form Nomad Investor letter 2006. Source Igy foundation website

What can Investors learn from Scaling Laws?

This might be the right way to think about scaling in organisms, but does it tell us anything about companies, and especially firms as they grow? The question that needs to be answered is: why is it predictable that a business will grow from a mouse to an elephant? This is a little like asking the meaning of life, and we will try hard not to give an answer as intractable as Douglas Adams’ suggestion in The Hitch-Hiker’s Guide to the Galaxy (where the answer to life, the universe and everything was “42”!). Several tenets are important. A business ought to be able to self-fund its own growth, and if the opportunity set is large, then the return on capital needs to be suitably high. Second, barriers to entry should increase with size; that way a company’s moat is widened as the firm grows. To do this, the basic building block of the business, its skeletal structure, is probably best kept very simple. In short, we want a skeletal structure that can support growth from mouse to elephant without too much skeletal reengineering.

Let’s consider traditional high street retailing. Goods are sent from the supplier to the retailers’ central warehouse, where they are stored until demanded by the shops. Goods are then sent to the high street stores. These are expensive pieces of real estate and have high operating costs. Price aside for a moment, the quality of service the consumer perceives is largely a function of staff levels, staff helpfulness, product range, shop furnishings and so on. So, there are lots of constantly variable elements to service quality at the most expensive end of the distribution system. It seems to us that the skeletal structure is highly complex, and many things can go wrong.

Contrast this to the internet model. Goods are sent from the supplier to a central warehouse, but often only after the order has been taken. The goods are then sent direct to the customer with the expensive high street real estate missed out. The quality of service perceived by the customer is the speed of delivery, the feel of the web site, functionality of the web site (such as recommendations), breadth of product range and so on and these factors are inherently more controllable. They are fixed in terms of expense and also customer experience (a web site viewed in New York looks the same as the same website viewed in London or Hong Kong). So, whilst quality is inherently patchy at most high street retailers, it is fixed at Amazon. This is important as it is complexity that is one of the main reasons firms fail as they try to grow.

It seems to us that the basic building block of internet retailing, its skeletal structure, is far more robust, scalable and cheaper than the high street equivalent. In other words, its power law is very high, and implies that businesses with the simplicity of operation as say, Amazon.com, have a shot at being far bigger, quicker and more profitable than their high street equivalents. Nomad has an investment in Amazon for more reasons than the firm’s simplicity of operations. But when this basic building block is combined with the scale efficiencies shared model (which increases the moat as the firm grows), customer centric orientation of the firm’s founder, as well as his healthy disdain for Wall Street, this combination makes us think that we may have a mouse that can turn into an elephant. To those who argue Amazon is large already we ask two questions: what do you think e-commerce will be as a proportion of US retailing in ten-years’ time, and what do you think it was last year? Write both numbers down and turn to the end of this letter*** for the answer to the second question. See below

*** The US Census Bureau estimates that e-commerce sales grew from 2.7% to 3.1% of all retail sales in the United States during the quarters of 2006. The source document can be found at www.census.gov/mrts/www/data/html/07Q1table1.html.

Disclaimer

This document does not consist of investment research as it has not been prepared in accordance with UK legal requirements designed to promote the independence of investment research. Therefore even if it contains a research recommendation it should be treated as a marketing communication and as such will be fair, clear and not misleading in line with Financial Conduct Authority rules. Holland Advisors is authorised and regulated by the Financial Conduct Authority. This presentation is intended for institutional investors and high net worth experienced investors who understand the risks involved with the investment being promoted within this document. This communication should not be distributed to anyone other than the intended recipients and should not be relied upon by retail clients (as defined by Financial Conduct Authority). This communication is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose. This communication is provided for information purposes only and should not be regarded as an offer or solicitation to buy or sell any security or other financial instrument. Any opinions cited in this communication are subject to change without notice. This communication is not a personal recommendation to you. Holland Advisors takes all reasonable care to ensure that the information is accurate and complete; however no warranty, representation, or undertaking is given that it is free from inaccuracies or omissions. This communication is based on and contains current public information, data, opinions, estimates and projections obtained from sources we believe to be reliable. Past performance is not necessarily a guide to future performance. The content of this communication may have been disclosed to the issuer(s) prior to dissemination in order to verify its factual accuracy. Investments in general involve some degree of risk therefore Prospective Investors should be aware that the value of any investment may rise and fall and you may get back less than you invested. Value and income may be adversely affected by exchange rates, interest rates and other factors. The investment discussed in this communication may not be eligible for sale in some states or countries and may not be suitable for all investors. If you are unsure about the suitability of this investment given your financial objectives, resources and risk appetite, please contact your financial advisor before taking any further action. This document is for informational purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned in it. Holland Advisors and/or its officers, directors and employees may have or take positions in securities or derivatives mentioned in this document (or in any related investment) and may from time to time dispose of any such securities (or instrument). Holland Advisors manage conflicts of interest in regard to this communication internally via their compliance procedures.