")

This letter is not part of the fund prospectus or offering documentation of VT Holland Advisors Equity Fund. Opinions expressed below are only those of the manager and shared for the interest of readers only. Qualitative terms like ‘great’ and ‘compounding’ are used only to explain the managers investing approach. Readers are instructed to look at the full disclaimers and fund prospectus.

Interim Investor Letter – June 2025

Dear Investors and Friends,

The fund NAV is up 6.7[1]% year to date as of 30th June and is now c.£40m in size.

This spring we made an important hire at Holland; Martin Weisinger joined us in a fund sales role. Martin is super experienced in this area and a really nice chap. These things don’t always come together I’ve noticed so I hope we have hit the jackpot. Martin has hit the ground running, so we are not going to be c.£40m for very much longer I suspect.

We write at length to our fellow investors twice a year. In these letters we lay out our investment approach in some detail. All those past letters are publicly available on our website. Those wanting to understand our investment approach from scratch would do well to read our 2023 year end letter and take a look at the slides from our 2025 investor day. As this is an interim letter, we assume readers already know our approach reasonably well.

The political and stock market volatility seen in the first half of 2025 has been discussed ad nauseum. Such volatility/market cycles, however caused, we see as business as usual for us as asset managers. During the spring market falls we added to existing holdings at lower prices (TSMC, Greenbrick). We also started new positions in PDD and Rosebank. The other big feature of this six-month period was the weakness in the US dollar. It was down c.10% vs sterling resulting in c.5% headwind to our NAV.

Supernatural Compounders – In search of Nirvana

We wrote a piece last year using the above title. It outlined how we might identify very special businesses assessing when to pay a higher price for their stronger growth. Many investors with a value bias are so set against MAG7 type companies that they miss an important point. This being that c.50% of total global stock market wealth creation in the last 30 years came from just the top 0.2% of companies (that is 160 out of 60,000 companies)[2].

Whilst we are Buffett fans and indoctrinated with Margin of Safety thinking, this observation is important. It should open our minds to try to find just one or two of these companies – who could be powerful drivers of future investment performance. That is what we are trying to do in this arena. In our December letter we profiled Wise Plc which we think is one such company. Another company we bought last year using the same thinking was Nu Holdings. We explain why a little below:

Nu Holdings ($13: $62bn MCap) – A Scale Economy Shared Disruptor

Around 18 months ago now we discovered Nu Holdings. Its low unit-costs, customer obsession and disruptor mindset in the lazy world of consumer banking immediately sparked our interest.

Simply put Nu Holdings has the best unit costs in global full service banking (75% below peers and still falling). It uses these low costs not to boost profits but instead to offer customers better interest rates (e.g. Nu’s 12% Mexican deposit rate vs c.5% offered by peers). Because of this and its high customer service focus, Nu is rightly loved by consumers. This can be seen in the speed with which 118m customers have flocked to it but also in its great Net Promoter Scores (NPS).

The global banking industry consumer offering has not really changed much in 50 years. (Accounts, loans, branches, poor interest rates, little customer service or value for money and add-on digital apps). We think that might be about to change.

Companies like Wise will tackle niches like foreign exchange, but Nu can offer a far more efficient full suite of banking products at great prices. Importantly its offering uses the Scale Economy Shared business model that we admire and seek out. We remind readers that it is this business model which has proven so powerful in retailing (Costco) and online (Amazon). Of course, there is a way to go before Nu can be included in such a rarified list of proven Gorilla businesses, but we think it has a good chance of success. We think Nu has the right building blocks and culture in place to challenge not just banks in Latin America, but globally.

Nu has real dedication to low-units costs combined with a desire to innovate and share such cost efficiencies with its customers. It is also obsessed with delighting the customer. These traits when combined create a powerful flywheel model that has been super successful in other industries and geographies. No one (except Wise) is trying to take this model into financial services, until now.

All this is symptomatic of the disruptor business models we seek out and what we look for in a business model with a long runway of growth. Indeed, when we wrote about ‘Supernatural Compounders’ in our Nirvana piece, Nu was at the forefront of our mind. In our recent investor meeting we listed six traits we look for in such a business (Nu possesses all six):

- A visionary founder

- Who re-thinks their industry – solving a hard problem

- …to give customers a more compelling offering

- Is low unit-cost driven and customer obsessed

- Has a huge runway of growth ahead

- Makes good/great ROICs that enable self-funded growth

Two further points interest us about Nu. The first is the giant scope of growth in front of it as arguably the whole global banking industry is ripe for this type of disruption. The second is how much the company’s current earnings are depressed, suggesting the shares are not as expensive as they look.

Counter positioning

The banking competitive environment has changed little in the last 40 years. There have been payment disruptors (Wise/Revolt), but not that much disruption of the core banking franchise. The scope and scale of what Nu have achieved in Brazil is important and telling. Big European and US banks we are sure have noticed, but crucially the actions they could take, were Nu to park its tanks on their lawns, may be quite limited.

To compete with Nu, incumbent banks will need future cost bases that are c.75% lower than today’s and more importantly a management mentality that passes much of that new efficiency on to customers. This would mean a re-basing of profits to much lower levels. From today’s starting point of incumbent bank culture and customer/shareholder relations this will be almost impossible to achieve.

Our confidence in this statement comes from our observations in so many other sectors that have been disrupted in this way (UK pubs, ecommerce, supermarkets, airlines, streaming). No matter how high the IQ is of incumbent banking CEO or how good the hired consultants are, the end result is so often the same. The list below captures the reactions industrial incumbents usually go through when confronted with a disruptive new entrant:

The five stages of grief

- Denial

- Anger

- Bargaining

- Depression

- Acceptance

Readers may highlight differences between Brazilian/Mexican banking vs other countries, thus implying our simple extrapolation of Nu’s model is maybe flawed. There are always regional and sector differences, but customer desire for ‘value for money’ is a philosophy that is both timeless and travels the world over – of that we are certain. We also note how powerful and well established the banks in Brazil Nu competed with to win its 100m customers were (e.g. Santander and Bank Itau). In short, we think Nu has the brand, customer service, culture and low unit cost base to win market share in many, many, countries.

The company’s recent commentary on its potential for global growth is interesting. They know they need global, not local IT systems to export their model worldwide. These take money and time to build. Nu are expensing such future growth costs today and tell us they should be ready by 2026/7.

Not only do we think Nu has a long runway of growth ahead of it we think it is already the best banking business model in the world today. A recent Nu investor presentation showed the group’s ROE of 27% (but this includes early stage set up costs in Mexico and Columbia). This 27% level is also calculated off a central capital base that is way in excess of the bank’s long term needs. Adjusting for such excess capital (and start-up costs) Nu’s ROE is c.60%. Remember this is a bank, a fully regulated and capitalised bank, not just a payment platform.

Depressed earnings

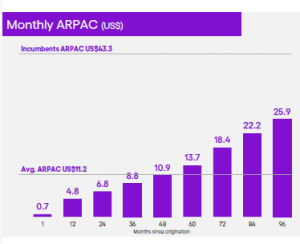

The most recent Q1 25 net income reported by Nu was $557m, annualised $2.2bn. This is the figure used in the 27% ROE calculations above. It also suggests a headline valuation of 28x PE. Readers might therefore assume all future growth is fully priced in. We do not agree. The chart below shows the ARPU[3] the company earns from each user of $11.2 (per month). It also shows that the average mature Brazilian bank has an APRU of $43. The longer customers have been with Nu the higher their ARPU (as they use more products).

Fig.1: Nu’s ARPU set to rise as customers mature

Source: Nu Holdings Q1 25 Results

Source: Nu Holdings Q1 25 Results

With super low and stable unit-costs each dollar increase in ARPU is highly profitable to the company. Particularly so, when such growth is just driven by existing customers maturing in their relationship with the company. At a c.60% incremental profit rate were the company’s ARPU to be $15 not $11.2 its annual profits today would be $4.8bn not $2.2bn. Adjusting for this reduces the Dec24 PE from 28x to 13x. Remember this is a historic multiple for a company growing 25-40% pa. Also, one with a runway to keep growing at similar rates for many years into the future. Despite its rapid growth to date, the company still only has a tiny market share of banking gross profit pools in Brazil (5%) and Mexico (<1%). This provides a glimpse as to how big Nu’s profit pool might be just by deepening its existing market positions. Future expansion in other geographies only expands its growth runway further.

Owner Manager

We think Nu a powerful future global business deploying a proven disruptor model. It is also led by its founder (David Velez). He is a perfect example of the sort of leader we wish to align our capital with. Visionary, ambitious and passionate about the right things. He always talks about:

- Lowest unit costs

- Outstanding customer service

- Great product innovation

- Developing an excellent culture

Disruptor businesses like Nu are, by definition, hard to forecast and much can change along the way. But we are in the probability game, not the certainty game. How high a probability do we attach to the idea that Nu might be able to carry on growing at high rates for a long period? And what price might we pay for a chance of such an outcome?

- Nu’s look through PE (using a more mature ARPU) is c.13x we suggest.

- Very prudently we could assume it will trade on a similar multiple 20y out (Likely more if it were still a dominant growing business with good products and ROE’s)

- If so, our investment return will match the compounding the company itself achieves

- So how fast might the company grow?

- Maybe today’s ROE (of 30-50%) will moderate to 25%

- If all of that were reinvested for growth at similar rates of return, then…

- The entity we own a portion of could grow at c.25%pa

- A quick glance of a compound interest table tells us…

- That at a 25% growth rate each £100 invested in Nu Holdings today will be worth…

- … £8,600 in twenty years’ time

We hope you can see why we are excited about our investment in Nu Holdings. We will leave the last words to Peter Lynch (see Appendix below).

With best wishes for an enjoyable summer.

Andrew J. Hollingworth

Fund Manager

Appendix

Peter Lynch on seeing the potential in growth businesses and the mistakes not to make.

“I don’t think that with great stocks you need a super-computer or an advanced Sun microsystems to figure out the math.”

Take the example of a company I missed: Wal-Mart. You could have bought Wal-Mart ten years after it went public. Let’s say you’re a very cautious person. You wait. Now ten years after it went public, it was a twenty-year-old company. This was not a start-up. So it’s now ten years after the public offering. You could have bought Wal-Mart and made 30 times your money.

The reason you could have done that is that ten years after it went public, it was only in 15% of the United States. And they hadn’t even saturated that 15%. So you could say to yourself, now what kind of intelligence does this take? This company has minimal costs, they’re efficient, everybody who competes with them says they’re great, the products are terrific, the service is terrific, the balance sheet is fine, and they’re self-funding. So you say to yourself, why can’t they go to 17%? Why can’t they go to 21%? Let’s take a huge leap of faith: why can’t they go to 23%? All they did for the next two decades was roll it out. They didn’t change it. I only wish they had started out in Connecticut instead of Arkansas. Source: Peter Lynch interview 2002

Mistake number 1

The first is waiting to buy the stock when it looks cheap. Throughout its 27 years rise from a spilt adjusted 1.6 cents to $23, Wal-Mart never looked cheap compared with the overall market. Its PE also rarely dropped below 20, but Wal-Mart’s earnings were growing at 25-30 percent a year. A key point to remember is that a PE of 20x is not much to pay for a company that is growing at 25 percent.

Any business that can manage to keep up a 20 to 25 percent growth for 20 years will reward shareholders with a massive return even if the stock market overall is lower after 20 years.

Mistake number 2

The second mistake is underestimating how long a great growth company can keep up the pace. In the 1970’s I got interested in McDonalds. A chorus of colleagues said golden arches are everywhere and McDonalds had seen its best days. I checked for myself and found that even in California where McDonalds originated there were fewer McDonalds outlets than there were branches of Bank of America. McDonalds has been a 50 bagger since. Source: Peter Lynch interview 2002

Please see full disclaimer below. This is not investment advice. The author is just sharing his opinion on a holding of the fund to give readers insight into his analytical thinking.

The information in this document is based upon the opinions of Holland Advisors London Limited and should not be viewed as indicating any guarantee of returns from any of the firm’s investments or services. The document is not an offer or recommendation in a jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such an offer. The information in this Report has no regard to the specific investment objectives, financial situation or particular needs of any specific recipient and is published solely for informational purposes and is not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. In the absence of detailed information about you, your circumstances or your investment portfolio, the information does not in any way constitute investment advice. Potential investors should refer to the relevant Prospectus and Key Information Investor Document for full information. If you have any doubt about any of the information presented, you should obtain financial advice. Past performance is not necessarily a guide to future performance, the value of an investments and any income from them can go down as well as up and can fluctuate in response to changes in currency exchange rates, your capital is at risk and you may not get back the original amount invested. Any opinions expressed in this Report are subject to change without notice. Portfolio holdings are subject to change and the information contained in this document regarding specific securities should not be construed as a recommendation or offer to buy or sell any securities referred to. The information provided is “as is” without any express or implied warranty of any kind including warranties of merchantability, non-infringement of intellectual property, or fitness for any purpose. Because some jurisdictions prohibit the exclusion or limitation of liability for consequential or incidental damages, the above limitation may not apply to you. Users are therefore warned not to rely exclusively on the comments or conclusions within the Report but to carry out their own due diligence before making their own decisions. Authorised and regulated by the Financial Conduct Authority (UK), registration number 538932. All rights reserved. No part of this Report may be reproduced or distributed in any manner without the written permission of Holland Advisors London Limited. Investment Manager: Holland Advisors London Limited (registered number 538932), registered office The Halt, Smugglers Way, The Sands, Farnham, Surrey, GU10 1NB.

- I class units ↑

- Bessembinder stock market study 1990-2020 ↑

- ARPU – Average Revenue Per User (monthly) ↑