Ryanair – Born to run

June 2024 (€17.2)

Ryanair’s share price and the odd financial metric suggest to some we are nearing the end of its profit recovery. We disagree. A reference point of future profitability Ryanair’s management gave investors a year or so ago was to make €10 of net profit per passenger (NPPP). Slavishly, all analysts made this output a crutch for their profit recovery forecasts. With a net profit per passenger in the period just reported (March 24) of €10.43, many seemingly assume this is the end of Ryan’s recovery. As the company also guides for slower growth in passenger fares this summer does this all suggest such investor caution might be warranted? In a word… No!

Core thesis. Unchanged and room to run

Our long-term bullish thesis on Ryanair was never predicated on any short-term profit recovery. It was driven by our admiration for its super low unit-cost model and the long-term earnings power we saw deriving from it. In Ryan’s case its lowest unit cost model we concluded was powerful for two reasons:

- It had almost no EU competitors to threaten it

- The model was being implemented by a talented, decisive and highly aligned owner manager. As we enter the pay-off stage in Ryan’s story we want to repeat a mantra we used a lot a few years back for fear readers may have forgotten it: Operate, Generate, Allocate. We want the companies/managers we invest alongside to excel at all these traits. Our c.10years study of Michael O’Leary (MOL) not only suggests he excels, but we conclude he is likely one of the best CEOs we have ever come across.

Before considering todays outlook for Ryanair shares some of these core assumptions are worth reflecting on:

Competitors and investment phases

Maybe a key difference between our assessment of Ryanair and that of other investors derives from the work we did on the industry long before Covid arrived. For years we had heard MOL talk of wanting to ‘kill off’ competitors. We even wrote a research piece entitled “To hell with yields”. This being a quote from MOL as he actively sought to depress pricing year after year to inflict pain on competitors and thus gain market share. This is why Ryan’s average fare fell from €46-48 in 2012-2014 to €37-39 in 2017-9. Inflation in those five years was not the level it is today, but costs were still rising. Anyone that has built an airline profit model and moved fares (in true isolation) up, or down by c.25% knows the impact of such a move. It is either Nirvana or Armageddon. Crucially, in western Europe Ryanair has almost no true low-cost competitors. This means that the decision to trash fares as it did to fill its planes and win share was a self-imposed investment phase. It was not a function of wider market behaviour as occurred in the US airline industry. During this period Ryan’s profits still grew but did so due to very low unit costs and full planes at low fares. Meanwhile its competitors suffered severely, gradually failing one by one.

Then Covid hit… Then interest rates rose. The result of which has been to turbo charge this entire capital cycle process. I.e. airline competitors that were struggling went bust quickly (Norwegian). Airlines with cost bases that were uneconomic (Al Italia, TAP Portugal) went bust a little more slowly. Most others curtailed growth (easyJet) or sought bailouts to survive (Lufthansa). As we observed in Holland Views: Ryanair – Second order thinking, May 2020 slower growth means higher unit-costs and bailouts come with conditions (i.e. no job losses or pay cuts). If you are flying 21% more passengers than you were before Covid, as Ryan is, then some cost inflation can be offset by scale (i.e. unit costs can be controlled). If like Lufthansa you are flying 18% less passengers in 2023 than you were pre-Covid, any cost inflation makes your unit economics even worse.

Lufthansa’s division profits reported an almost record 7.2% EBIT margin in 2023. With costs up and traffic down how did they achieve this? Short haul fares were 11% above 2019 levels, but long haul fares were 28% above 2019 levels! There are many ways to look at this, but we think it illustrative of how a company on the wrong end of unit-cost inflation is forced to make its product very expensive to restore profit margins.

Does the above suggest that Lufthansa has pricing power in its long-haul traffic? Well, only until such time as a long haul competitor can get slots on its direct routes. Greedily pricing a monopoly position like this with a likely inflated cost base hoping no new entrant turns up to undercut you is not, in our view a good long term businesses model. Maybe it could be seen as a melting iceberg.

Inflation meets pricing power

Alternatively, ensuring you have the lowest costs possible and passing much of that low-cost efficiency onto customers is a powerful, sustainable, self-reinforcing business model. This is Ryan’s model. Companies with such business models are often slow to increase prices, due to their customer value focus. As such pricing power might not seem evident (JDW is a good current example) but that does not mean they do not possess it.

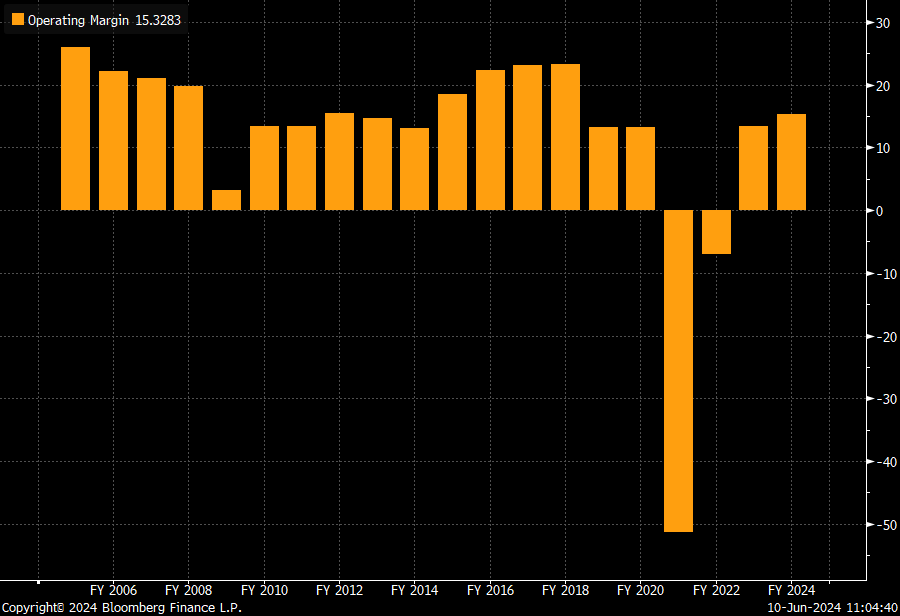

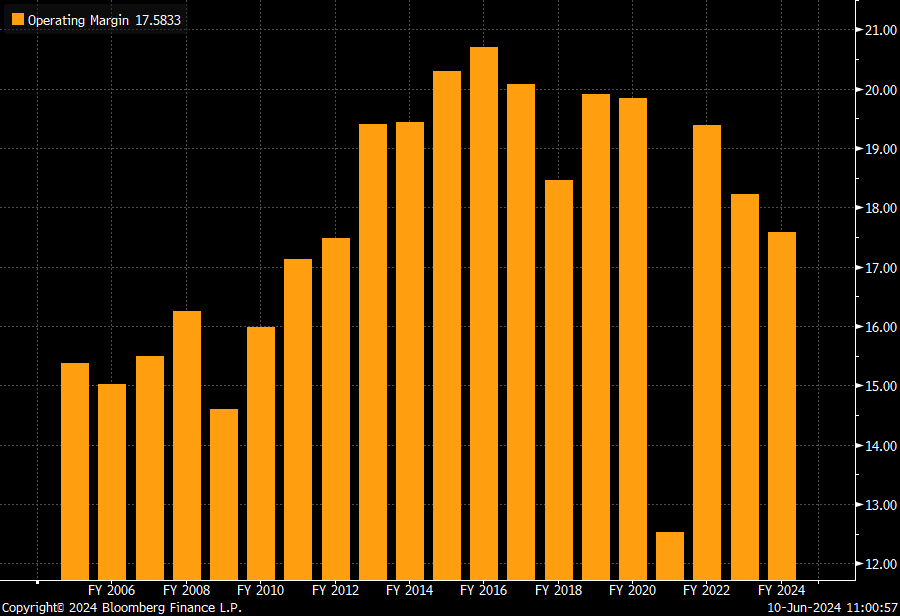

Fig.1: Ryanair EBIT Margin

Source: Bloomberg

Source: Bloomberg

At any moment in time Costco could increase its gross margin by 2% and likely its LFL sales would not suffer. It does not choose to do so however as it knows keeping its customer value proposition strong ensures they return year after year. Whilst this analogy is fair for Ryanair’s longer term offering, it belies periods of investment or cyclical downturns that can overlay a core value offering. Costco has not really had such a period, but Amazon has, resulting in margin (and share price) falls.

The crux of difference in our vs other investor’s view on Ryanair is that we think the company was in a heavy investment phase before Covid-19, evident in its heavy fare discounting actions.

Fig.1 shows Ryanair’s EBIT margins (15% today vs 22% of past peak). The Appendix shows the EBIT margins of Next, Greggs and Lufthansa. All of whom have recovered pre-Covid-19 margins fully. Companies such as Greggs or Next have kept their customer proposition competitive but have passed on cost inflation. Thus, their pricing power can be seen in the fact that they have sustained EBIT margins. The above Ryan chart suggests that unlike Greggs, Next or Lufthansa, Ryanair may not have the same pricing power as it did in 2016-18. We disagree. Ryan, today we think has more pricing power than at almost any time it its history. It is just about when it chooses to use it. Like all good scale economy shared businesses Ryanair have never sought to profiteer from short term pricing pops. Instead, they have just pushed and pushed the relative cost base of the company further down and then filled their planes, letting clearing prices for fares determine their margin. So as others now have to pass on cost inflation in needed higher fares, Ryan is a natural beneficiary. This has been the driver of industry short haul pricing in the last two years and of the recovery in Ryan’s profits to the level we see today.

Investment phase – Where are you?

Farming cycles of seeding and harvesting are well known. Far less consideration is made for the cycles that companies go though. We have written at length about the capital cycles that certain industries experience and how powerful they can be when they end (Holland Advisors: Netflix – The Discovery Channel, April 2023). But companies can also go through heavy muti-years investment phases of their own choosing. This we observed at Frasers as the company re-invented itself over a five year period moving away from discounting. A very early observation we made at Frasers ended up being right. This was that the company should, by rights, end up a higher margin business when it emerged from its investment period. This was based on the simple premise that heavy discounting hurts margins, so less discounting net net will result in higher margins than the past. Crucial to this observation was the assessment (by us and Mike Ashley) that there was not a competitor waiting in the wings to undercut them:

“Where else are they going to go” Mike Ashley in investor meeting c.2019

Hopefully readers are seeing the read across we are making. Ryanair invested very heavily in price discounting over a period of years to inflict pain on competitors. That period is now largely over. As such when addressing our “where are you?” question to Ryanair, the answer is they are entering harvest time/are past the heavy investment period. Despite the investment made in lower fares, during the period 2016-2018 it still made €12 net-profit-per-passenger and reported c.23% EBIT margins. These financial outputs were a function of more unit sales, low unit-costs and discounted fares. As with our Frasers work, slightly less discounting in future surely should lead to higher margins in time. That Ryan’s most recent year EBIT margin are 15% not 23% suggests this thesis (if correct) has a way to run.

A crucial insight into the future of Ryan and its likely profitability has come from our discussions with MOL. On each occasion we have met with him we have only discussed the end game for the company, i.e. what things will look like once the majority of competition-killing pressure has been inflicted. MOL, first privately and then more openly, has discussed what this endgame looks like. It implies a record high level of profitability, but one derived from scale and an unmatched cost base, not from short term price increases.

“A level of NPPP of €10 feels very modest. €10-€15 feels like a better/more likely range” Eddie Wilson, Ryanair Investor Meeting, Nov 2023

The love of winning – not just the game!

Whilst the company will never be undercut on price MOL (like Mike Ashley) is acutely aware that less discounting is great for margins. Once the company has achieved a desired scale of market share in most western European countries it will grow capacity more slowly than its past. Indeed this maturing/moderation of growth is already forecast (see below). The end result of which will be continued dominance with locked in lowest unit-costs, but also likely better profitability due to less discounting. A final point of conviction for us comes from hearing the joy this highly profitable endgame brings to MOL. This is not a man running a company just for the thrill of bringing low fares to the world. This is a man that really understands the power a super-low unit cost business can have and the scale of the profit it can produce at maturity.

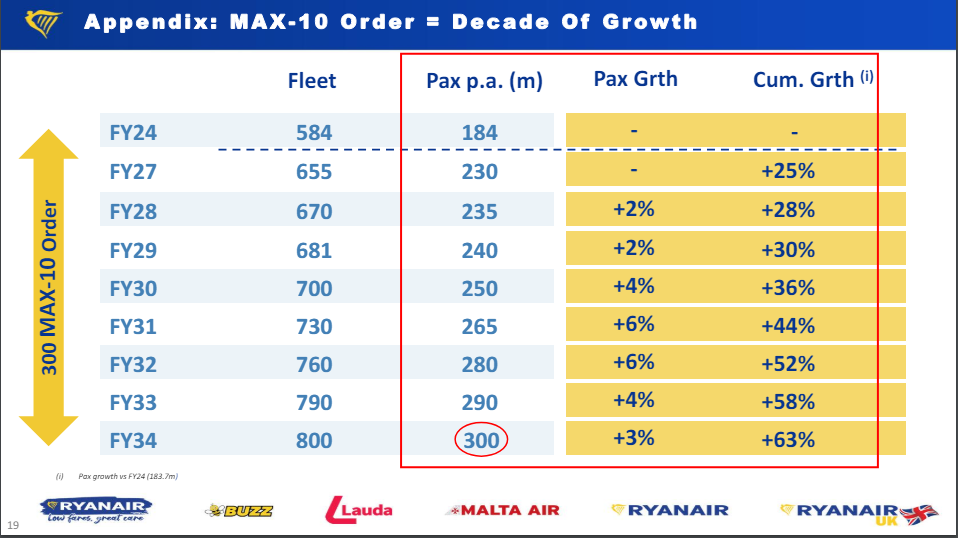

Fig.2: 300m passenger target for 2034

Source: Ryanair Full Year Results, March 2024

Source: Ryanair Full Year Results, March 2024

Higher staff costs and indeed future new plane depreciation costs all can/will lead to higher airfares. The crucial bit from an investor’s perspective is what part of higher fares (if any) can be retained by a company in its profitability. The last few years have seen a rebuilding of profits in this sector as some air fare rises were retained. Ryan’s EBIT margin in the year just reported was 15.3%, easyJet’s was a far more modest 5%. What margins Lufthansa makes short haul we are not told, we suspect it is not much. These competitors’ low margins are instructive. They show that the fares increases across the industry thus far were not profiteering, but just done for financial survival. We must also remember that the huge absolute gap between Ryan’s pricing (average Ryan fare is €50 vs easyJet €81) is still in place. So whilst Ryan’s fares may have risen, its customers are still getting great value.

Allocate, allocate, allocate

When reporting to shareholders in autumn 2023 Ryanair reminded investors that it had returned €6.7bn to shareholders in the period 2008-2020. This can be easily calculated as c.70% of the net income the group produced in those twelve years. This is a reiteration of the exact calculation we made a few years back. What we noted at the time was an important additional observation. This being that whilst making ROE’s of c.20% Ryan also grew passenger numbers c.10%pa. The financial wizards in our readership might cry foul. A company that needs assets to grow must require 50% of profits to be retained to grow at 10% pa (i.e. 20%*0.5= 10%). The reason Ryan was able to grow and pay out 70% of net income was due to its sizable and ever growing negative working capital.

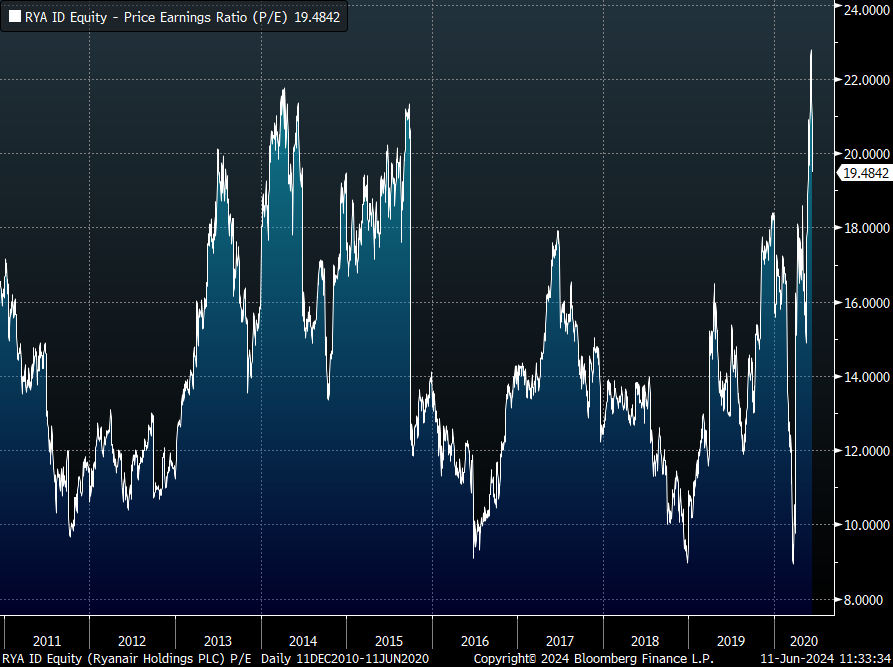

During such years 2010-2020 Ryanair shares traded in a PE range of 12-20x earnings (see Appendix). In part this reflected the growth of the business and its cyclicality. It also reflected that 70% of earnings were being distributed while the company grew. Whilst a future lower multiple might be argued for by some, we are not inclined to agree. Ryan’s current and future position is one of far more assured sector dominance than was the case 10-15y ago. Record high margins and just an eye to yield management vs trashing fares to hurt competitors we think a far more attractive prospect to many investors. We have suggested above that the company’s future margins can at least match those of its past. We are inclined to feel the same about its valuation. We suspect Mr Market might pay at least as good a multiple for a mature, sensible, highly profitable and cash generative market leader as it did the maverick upstart of the past.

A look forward

Projecting cost and fare inflation independently is what analysts feel they need to do. But higher or lower fuel will in time be reflected in fares, as will higher or lower staff, plane and airport landing costs. What ultimately drives profitability is the relative position vs peers and the spread of revenue vs cost that your business model/unit cost leadership allows you over time to earn. +/- what you then choose to re-invest. If we are happy to conclude that Ryan’s market power today is as at least as good as its pre-Covid past then we can do as we did with Frasers, i.e. value the business off of a return to past peak margins (not more).

A little maths

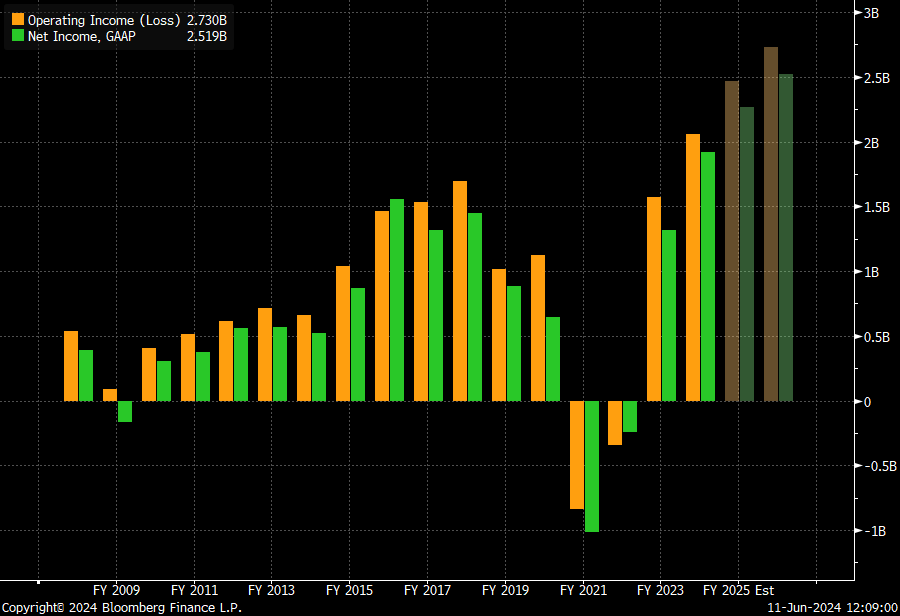

Fig.2 above shows Ryan’s cumulative +64% growth in passengers projected over the next 10 years. If we also assume a c.3% pa rise in fares (mostly likely cost pass through) this adds a cumulative 34% rise in fares over those 10 years. Combined this gives a revenue increase of 97%, which for ease we will take as +100%. Just reported March 2024 revenues for Ryan were €13.44bn, thus we will postulate they might be €27bn in 2034. At a 22% margin the resulting EBIT is €5.9bn. The joy of Irish tax is that c.90% of Ryanair’s EBIT translates into net income. As such net income would be €5.3bn. A 14x multiple on which would imply a valuation of €74bn. The IRR on that value from today starting M.Cap of €19.5bn is c.15%.

However, we must remember MOL/Ryan’s past distribution of excess cash. Despite much slower passenger growth than the past we will assume that c.70% of net income is distributed (it could be more). As was the case in 2008-2020. We will assume today’s derisory PE of 8x rises to an average 12x over the period. The result being that in addition to the c.15% return investors look set to makes from the intrinsic value growth of the company, they will also make a further 5.8%pa in capital returns (100/12*0.7= 5.8%). All in investors look set to make c.20% IRR’s from owning Ryanair shares for the next 10years we suggest.

Observations on our maths

- We of course can see that the 22% EBIT margin we are using for Ryan is its peak past margin not its average. Indeed the company might not make 22% in 2034, but we would be surprised if at some stage between then and now such earnings power (or more) were not demonstrated for a year or two. Once Mr Market sees that and takes it onboard, we suspect a proper re-valuation of the group to occur. We note that peak past multiples (20x) coincided with peak margins also!

- Were we to use an 18% rather than 22% EBIT margin our investor IRR falls from 20% to 18% (12%+6%)

- A 22% EBIT margin implies a NPPP of €17.6. An 18% margin implies €14. These seem reasonable endgame scenarios to us

- If Ryan’s fares rise 3% pa over the next ten years, they will still represent excellent value for money for the travelling public. (€27bn of revenue for 300m passengers = c.€90 per passenger total spend) vs €73 today

- At the same time its increased scale (to 300m passengers) will have ensured it has kept a strong unit cost advantage over its peers

- Might Ryan of the future be more capital intensive vs Ryan of the past? This we note with a nod to large plane orders soon to start. With this in mind we asked Eddie Wilson just that in November. Here was his response:

“In the next ten years the company will be similarly capital intensive, similarly cash generative – with the same working capital as it has had in the last 15 years” Eddie Wilson, Ryanair, Investor Meeting, Nov 2023

March 2025 – A poor year!

Much has been made of the company’s communication of slower than expected fare rises during this summer. Ryan tells us that passenger volumes are likely to rise 8% and maybe fares only c.3%. Operating cost will likely follow passenger volumes as (including fuels savings) they look set to remain broadly flat in unit terms. Writing that out does not sound too exciting. The resulting 28% rise in EBIT is however perhaps more appealing! MOL in January talked of fares being up 5-10% this summer… likely he got just a little over his skis. That said, not a single analyst forecast had anything like such fare rises within it. If it did, it would have implied EBIT would be up c.75% in 3/26.

Our best guess of EBIT + 28% in this current year is a function of Opex +8% and revenue +11%, i.e. it shows what can happen when just a little more operational gearing is delivered upon. Dividend and buy backs will improve on that 28%, likely offering shareholders growth in value-per-share of >30%+. If that’s a poor year we will take it every time!

Under-earning AND Under-valued

One of the key tenants we look for in investments but don’t often see is to find a great business that is both underearning and undervalued. The great business bit does the top line compounding for us, but the under-earning and undervaluation, if both unwinding, can create powerful investor compounding. We think that has played out in our work in 2022/2023 on TSMC. That business is now once again making higher returns on more capital employed than when we first wrote on the company. Additionally (either by AI luck?) or our good judgement, Mr Market has re-assessed how it feels about the business. The result has been a doubling of the share price since our initial Dec 2022 work. Our TSMC pieces can be read here and here.

A week or two studying TSMC’s business models’ inputs and the outputs it has produced, suggests past higher valuation multiples given by Mr Market were largely justified. This being due to the huge moat this business has and the rare combination of growth with sustained high returns it can produce consistently. Today’s lower valuation occurring just as strong re-investment opportunities are actively being developed by the company thus looks compelling to us. Source. Holland Advisors: TSMC – What does Warren see, Dec 22 (US$80)

More often a business whose profit metrics (ROCE or margin) are depressed comes with a higher valuation on currently depressed profits as markets try to discount some sort of recovery. That is the situation we think CarMax shares, for example, are in today. When markets give up expecting a recovery and both margin and valuations are depressed huge bargains can sometimes be found. That was the situation we think Ryanair shares offered investors in 2022/2023. With the company having now achieved its first milestone of €10 NPPP many investors perhaps see it as having recovered, hence its low multiples (PE= 10x 3/24 and 8x 3/35). As our work laid out above hopefully illustrates, we think there is revenue growth, operational gearing and good allocation of excess cashflows yet to come. This underearning combined with a depressed multiple is a wonderful opportunity we assess. If you would rather listen to analysts near term forecasts you are welcome to, but we suggest you reference their past recent year accuracy on Ryan. They made c.50% revisions inside 12 months. See below:

Fig.3: Mr (and Mrs) Market’s Ryan’s Earning Forecasts

Source: Bloomberg

Source: Bloomberg

In summary

Our analysis and investing journey with Ryan has been interesting and educational. In the study of other companies worldwide we have learned that sometimes great value can lie in plain sight. Often this might be due to a combination of factors that we interpret as powerful, and others dismiss. The alignment of Zuckerberg as an owner-manager who in time would allocate Meta shareholder capital wisely we saw as unknowable in timing, but an indisputable outcome eventually. Our Ryan assessment is one where we think investors need to mix three skills, all relatively simple in isolation, but powerful when combined.

These are:

- A need to understand the resilience and power of a mature scale economy (lowest units cost) business model

- That even such businesses can have muti-year investment periods that can significantly depress profits/earnings power

- An ability to clear headedly calculate future operational gearing even when the outcome might seem outlandish

We think that is what we are doing and conclude as a result that we are being offered wonderful future compounding potential (IRRs of 20% for 10y) in a highly resilient, world leading business.

We could of course be wrong… only time will tell.

Links to most of our past Ryanair notes can be seen here.

With kind regards

Andrew Hollingworth

The Directors and employees of Holland Advisors may have a beneficial interest in some of the companies mentioned in this report via holdings in a fund that they also act as managers to.

Appendix

Greggs EBIT margins – Price rises ensured full cost pass through

Source: Bloomberg

Source: Bloomberg

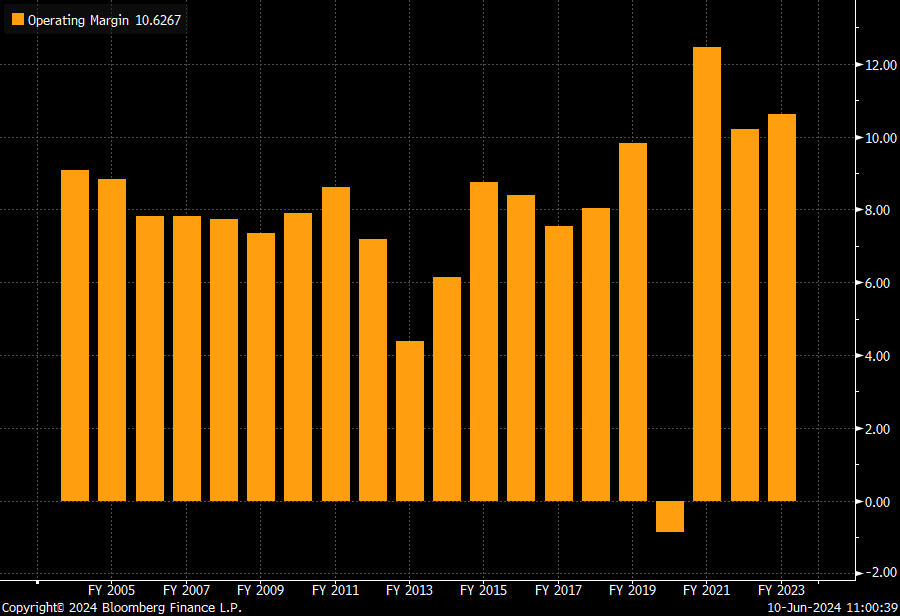

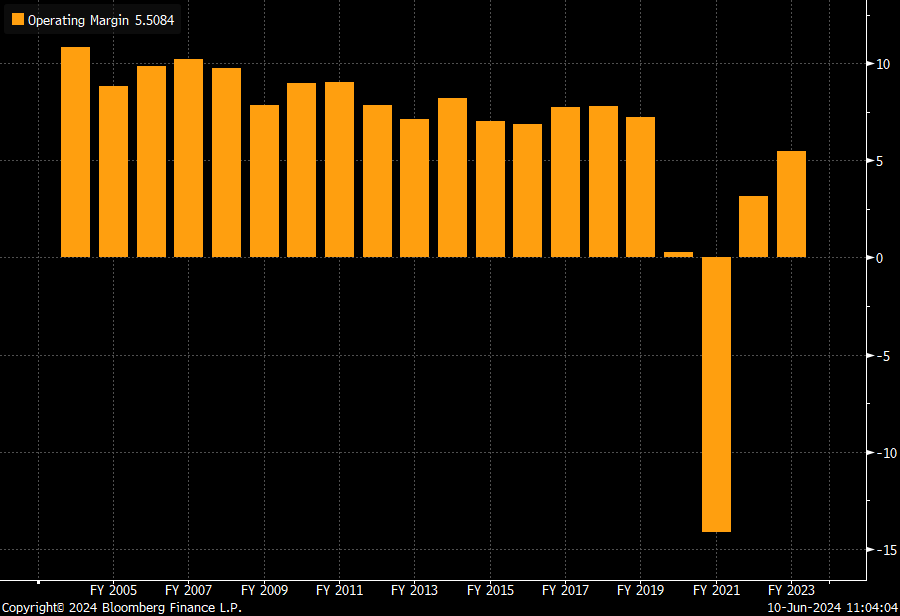

Lufthansa EBIT margins – at record highs

Source: Bloomberg

Source: Bloomberg

Next EBIT margins

Source: Bloomberg

Source: Bloomberg

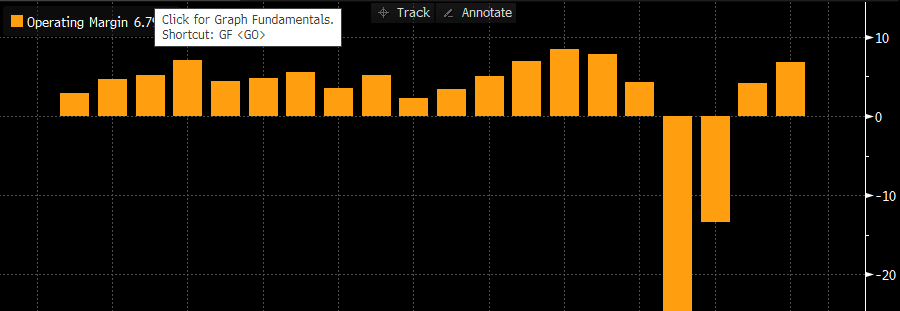

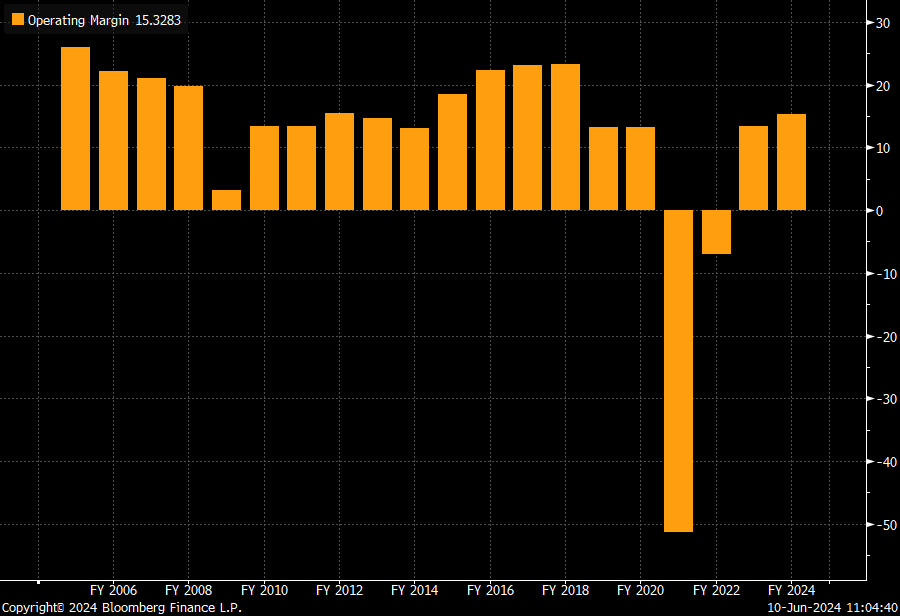

JDW EBIT margins – similar to Ryan… more recovery still to come

Source: Bloomberg

Source: Bloomberg

Ryanair EBIT margins

Source: Bloomberg

Source: Bloomberg

Ryanair 2010-2020 PE rating

Source: Bloomberg

Source: Bloomberg

Ryanair 90% of EBIT converts into Net Income

Source: Bloomberg

Source: Bloomberg

Disclaimer

This document does not consist of investment research as it has not been prepared in accordance with UK legal requirements designed to promote the independence of investment research. Therefore even if it contains a research recommendation it should be treated as a marketing communication and as such will be fair, clear and not misleading in line with Financial Conduct Authority rules. Holland Advisors is authorised and regulated by the Financial Conduct Authority. This presentation is intended for institutional investors and high net worth experienced investors who understand the risks involved with the investment being promoted within this document. This communication should not be distributed to anyone other than the intended recipients and should not be relied upon by retail clients (as defined by Financial Conduct Authority). This communication is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose. This communication is provided for information purposes only and should not be regarded as an offer or solicitation to buy or sell any security or other financial instrument. Any opinions cited in this communication are subject to change without notice. This communication is not a personal recommendation to you. Holland Advisors takes all reasonable care to ensure that the information is accurate and complete; however no warranty, representation, or undertaking is given that it is free from inaccuracies or omissions. This communication is based on and contains current public information, data, opinions, estimates and projections obtained from sources we believe to be reliable. Past performance is not necessarily a guide to future performance. The content of this communication may have been disclosed to the issuer(s) prior to dissemination in order to verify its factual accuracy. Investments in general involve some degree of risk therefore Prospective Investors should be aware that the value of any investment may rise and fall and you may get back less than you invested. Value and income may be adversely affected by exchange rates, interest rates and other factors. The investment discussed in this communication may not be eligible for sale in some states or countries and may not be suitable for all investors. If you are unsure about the suitability of this investment given your financial objectives, resources and risk appetite, please contact your financial advisor before taking any further action. This document is for informational purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned in it. Holland Advisors and/or its officers, directors and employees may have or take positions in securities or derivatives mentioned in this document (or in any related investment) and may from time to time dispose of any such securities (or instrument). Holland Advisors manage conflicts of interest in regard to this communication internally via their compliance procedures.