Becle SAB – Tequila Sunrise meets Capital cycle

Sep 2019 (MXN28)

- In a post MIFID world we think genuine idea generation is short in supply. Thus, we will try to share more of our ideas with clients without the need for always writing reports long hand. Rest assured we have done much background work on any idea we air, hence the extensive list of links we give at the end of this piece to aid your further research.

- Our daily quest for finding great businesses, priced-like-Ok ones continues. To remind you, we are looking for businesses with Franchise qualities that are under-earning and under-valued.

- Everyone knows that the best Spirits companies (Diageo, Remy Martin et al) are great businesses enjoying high margins (see Fig.2) and strong returns thanks to low input costs, excellent brands and strong distribution channels. As such it is rare to find a potential mispriced Spirits business with great brands. We think we have.

- That this is newly-listed (in Mexico) should not put you off. This is a world class spirits business with heritage brands, dominant market position and majority (85%) family ownership. It also has an ADR and a $5bn Mcap cap (but a limited free-float we accept).

- We have read extensively on this company; what follows is just our highlighted thoughts:

- Becle SAB is better known as the owner of 200-year old Cuervo premium Tequila brand. With c.43% of global market volumes it is the clear global market leader in premium Tequila (Becle also owns Bushmills Whiskey and Kraken rum). It also owns good US distribution assets to which it is committing more resource. It has only been listed since 2017 and investors will have to wait another few weeks for the first English translation of the report and accounts (we have been working off of an abbreviated version). This is not a well-known stock. It is down 20% from its IPO.

- Tequila, is analogous to Champagne in that premium quality Tequila must originate from a particular region in Mexico and be made from the Agave plant. This is important as you are about to see. Demand for Tequila has been very strong (volumes +7% cagr last 5 years), particularly demand for premium Tequila as the companies that control the top end brands (Becle and a Byron Trott controlled company interestingly) have successfully sold a premiumisation message. Ironically it is this strong demand that has thrown the tequila industry profits and in turn Becle stock off-course. This is the opportunity.

- Becle’s problem boils down to a temporary shortage of Agave (cactus looking!) plants in Mexico suitable for Agave juice production. This has had material implications as higher Agave costs have hit margins. Because premium Tequila uses twice the amount of Agave juice as regular tequila the sectors success in its premiumisation strategy has created a shortage of agave plants. Whilst Becle has the largest in-house source of agave plants of all Tequila producers, outside stocks have become much more expensive for it and competitors to source. Some product price rises have compensated (but a competitor brand owned by Suntory has been slow to follow suit). Equally more agave plants are being planted, but they take 6-7 years to reach maturity.

- We encounter all sorts of operational problems in our company research on a weekly basis and we are not being flippant here, but surely Cactus supply is down the list of serious long-term problems a 200-year old company with a wonderful brand might face?

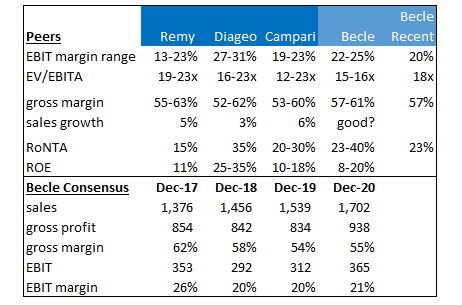

- On a headline valuation of 25x PE, Becle certainly does not look cheap at first glance, but importantly that is struck off a 2018 EBIT margin of 20% (vs. the 25-26% in recent years pre-IPO). Consensus forecasts are extrapolating recent depressed margins through 2020 as we show below. This is the crux of the investment case today. Company conference call Q+A reveals an analytical/investor community that is a little scarred post the profit/share price fall, but also one that is obsessed on forecasting when Agave GOGS costs will come down. Only then seemingly will they be more optimistic (6 out of 13 analysts that cover it have a “Sell” rating on the stock). We are however prepared to stand back from this issue and assert that:

- Cost inflation issues are rarely long-term drivers of margins in spirts companies

- Short term production difficulties are usually just that- short term in nature

- In time market forces will solve this problem, with either pricing increasing or the supply of Agave plants increasing – indeed Becle have admitted they have planted 20% more plants that usual in the last 2 years. (Our best guess is that both might occur, i.e. lower costs and better pricing)

- Capital cycles are a funny thing and in the case of agave plants a prickly thing! At the time of IPO Becle told investors of its plan to bring more agave production in house (currently it is at c.60%) but the recent super-boom in agave prices (up 6 fold in 5 years!) has likely lead to farmers being a little more flush, thus less inclined to sell their plantations. Becle has adapted accordingly, logically stating that its long-term intention is to still bring more production in house, but short term it is not paying up. We see that as a highly logical response; others seem to see it more like a U-turn..

Fig.1: Becle vs. Global spirit company peers

Source: Holland Advisors, Bloomberg – Becle forecasts in US dollars

Source: Holland Advisors, Bloomberg – Becle forecasts in US dollars

We suspect that as we write many Mexican farmers will be planting more and more of their crop of pure gold (Agave plants) to profit further from today’s super normal pricing. However, like many commodity capital cycles before it this will mean in c.5 years’ time, there will likely more than enough to go round. Seemingly for other investors that is too long to wait. By normalising Becle’s earnings power we think Becle shares are on offer for c12x 2020 EV/EBIT (This is comparing todays EV with the market forecasts we outline above adjusting for its EBIT margin to once again be 25%, not the 20% analyst expect). EV today of $5.1bn vs. 2020 EBIT at 25% margin of c.$425m = 12x. We accept that maybe investors have to wait longer than 2020 for 25% margins to be recovered to, but the math we hope is illustrative.

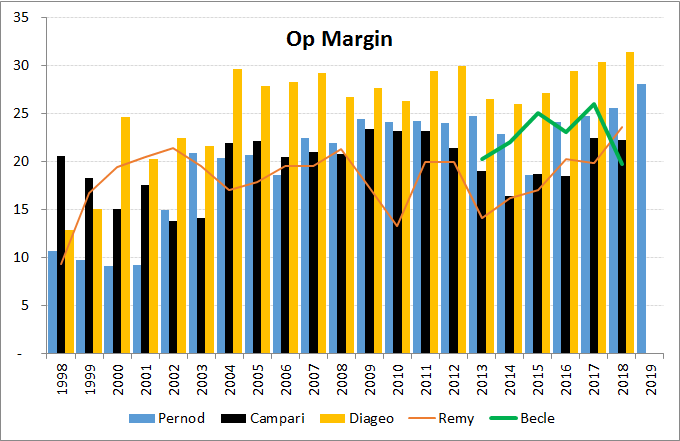

Fig.2: Global spirits companies Operating Margins

Source: Holland Advisors, Bloomberg

Source: Holland Advisors, Bloomberg

Peer group shows long term margin stability underpinning these businesses

This discussion is the nub of the issue and the key to understanding Becle’s current mispricing we think. We provide links below to publically available work discussing the input cost and supply chain issues facing the Tequila distillers due to industry Agave shortages. We strongly urge you to read these but we consider much of this ‘news noise’ in the face of not just Becle brands but also against this industry’s long-term profitability and the resilience of it, as illustrated in the chart above. This chart alone prompts a few other observations:

- Industry profitability has remarkable longevity attached to it (23-30% margins for 20y)

- That any investor just buying the shares of a profitability(margin) laggard would have done brilliantly (Campari in 2014, Remy in 2013)

The table in Figure 1 also shows Becle’s peers’ past profitability (i.e. margins) and the ranges of EV/EBITA multiples they have traded on in the last 10 years. What is notable at present is that almost every peer company is at its peak margin and peak multiple. That might not scream “margin of safety” in the shares of those companies, but it does show there could be good upside in both margin and multiple for Becle.

Interestingly whilst the data we have for Becle is only short its gross margins, EBIT margins and RONTA were all industry leading pre the Agave shortage issue. Looked at dispassionately this makes great sense, for they are the market leader in their spirit sub category (Tequila).

Additionally, in normal periods one might expect Mexican production costs to be lower than say those in Ireland or Scotland. Of course scale and distribution matters in this industry, and the peer companies have a myriad of brands, some dominant, some niche. But Becle is a dominant brand in its core market and has made significant investment in capacity both in its core Tequila business and at Bushmills.

A few other observations:

- Why did Becle float a minority stake? Is it likely they have been approached about selling the business in the past? Yes, very likely. Does a floatation stop such an acquisition happening or does it make it a free for all fight that could maximise value rather than a quiet private transaction? One day this company we think will likely be in the hands of a bigger global group, but that buyer will have to pay a very royal price to get it. We note only this week that Pernod paid no less than a 100% premium to get control of Castle Brands. We note how small the Becle float is and how it did not come with any debt. This was hardly a private equity sell down type transaction. Quite the opposite.

- Becle’s other two brands are very good quality in their space. Bushmills Irish Whisky and Kraken rum. Becle are currently investing capital to double Bushmills output capacity by 2022.

- Becle spends an industry leading amount of money on AMP (Advertising, Marketing and Promotion). Last year this was 22% of sales. Only Remy Martin spends as much. Diageo and Campari spend 10-15% of sales.

- Becle has no debt. Many of its peers are lowly levered too, but the EV/EBIT valuation we obverse above is all equity.

- Last, but not least there is an accounting quirk we are waiting for the answer to. The valuation stab we have made uses EBIT and EBIT margins. We do however note that in Mexican Peso (20 to the USD) accounts there was a sharp rise in the amortisation charge (from P283m in 2014 to P530m in 2018). We might find when we get the English full accounts (currently we are working off an abridged version) that these non-cash charges are helping to understate EBIT a little (by c.5% is our best guess).

Buts

There are of course few buts.

- The first relates to the Becle family and whether they will use their new share piece currency wisely or might make overpriced acquisitions.

- Secondly there is of course the fact that the company is quoted and reports its accounts in Mexican Pesos. We would not be surprised if in time that changed to US dollars. Current Peso reporting clearly brings in more currency risk and for many investors the spectre of political risk also.

We hope you found this outline of our view on a new company of interest. As selection of further reading attached will help you learn more.

Further reading links

- An informative investor case study on Becle[1]

- Value Investor Club write-up[2],[3]

- Becle’s corporate history[4]

- Article on the Tequila industry’s Agave shortages[5]

- M&A:

August 2019: Pernod Ricard acquires Castle Brands (Whiskey) for 100% premium[6]

January 2018: Bacardi acquires Patrón Spirits (Tequila) for US$5.1bn[7]

June 2017: Diageo acquires Casamigos (niche Tequila) for US$1bn[8]

April 2018: Byron Trott[9] acquires Casa Dragones (niche Tequila)

We have built a detailed historical model for this company and its peers – please ask for copies.

Kind regards

Andrew Hollingworth & Mark Power

The Directors and employees of Holland Advisors may have a beneficial interest in some of the companies mentioned in this report via holdings in a fund that they also act as advisors to.

Disclaimer

This document does not consist of investment research as it has not been prepared in accordance with UK legal requirements designed to promote the independence of investment research. Therefore even if it contains a research recommendation it should be treated as a marketing communication and as such will be fair, clear and not misleading in line with Financial Conduct Authority rules. Holland Advisors is authorised and regulated by the Financial Conduct Authority. This presentation is intended for institutional investors and high net worth experienced investors who understand the risks involved with the investment being promoted within this document. This communication should not be distributed to anyone other than the intended recipients and should not be relied upon by retail clients (as defined by Financial Conduct Authority). This communication is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose. This communication is provided for information purposes only and should not be regarded as an offer or solicitation to buy or sell any security or other financial instrument. Any opinions cited in this communication are subject to change without notice. This communication is not a personal recommendation to you. Holland Advisors takes all reasonable care to ensure that the information is accurate and complete; however no warranty, representation, or undertaking is given that it is free from inaccuracies or omissions. This communication is based on and contains current public information, data, opinions, estimates and projections obtained from sources we believe to be reliable. Past performance is not necessarily a guide to future performance. The content of this communication may have been disclosed to the issuer(s) prior to dissemination in order to verify its factual accuracy. Investments in general involve some degree of risk therefore Prospective Investors should be aware that the value of any investment may rise and fall and you may get back less than you invested. Value and income may be adversely affected by exchange rates, interest rates and other factors. The investment discussed in this communication may not be eligible for sale in some states or countries and may not be suitable for all investors. If you are unsure about the suitability of this investment given your financial objectives, resources and risk appetite, please contact your financial advisor before taking any further action. This document is for informational purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned in it. Holland Advisors and/or its officers, directors and employees may have or take positions in securities or derivatives mentioned in this document (or in any related investment) and may from time to time dispose of any such securities (or instrument). Holland Advisors manage conflicts of interest in regard to this communication internally via their compliance procedures.

- https://www8.gsb.columbia.edu/valueinvesting/sites/valueinvesting/files/pictures/Cuervo.pdf ↑

- https://www.valueinvestorsclub.com/idea/Becle_SAB_de_CV/7410195567 ↑

- https://www.valueinvestorsclub.com/idea/Becle_S.A.B._de_C.V._/7840919531 ↑

- http://www.fundinguniverse.com/company-histories/casa-cuervo-s-a-de-c-v-history/ ↑

- https://tastetequila.com/2018/agave-crisis-boom-bust-or-business-as-usual/ ↑

- https://www.businesswire.com/news/home/20190828005771/en/Pernod-Ricard-Acquire-Castle-Brands-223-Million ↑

- https://www.forbes.com/sites/noahkirsch/2018/01/22/bacardi-to-acquire-patron-tequila-for-5-1-billion-billionaire-owner-will-cash-out/#5a8661133590 ↑

- https://www.diageo.com/en/news-and-media/press-releases/diageo-to-acquire-super-premium-tequila-casamigos/ ↑

- Trott is the renowned advisor to Warren Buffett and John Elkann so his interest in the space is notable ↑