looks like (Part 1)")

What a capital cycle peak (AI) looks like (Part 1)

June 2026

AI is a capital cycle, and it has all the hallmarks of a big one. How to understand it and invest with care during its full length is something I have spent much time reflecting on in recent months. Many new to the investing game (those under 50) will see this as an amazing new chapter for the world where everything changes. There may well be some truth to that, but what is equally true is that much of the industrial and investor behaviour (and crucially how these two interact) we have seen many times before. In this piece I share my lessons of the past. In the next we will try to look forward.

An AI bull, but have seen this movie before

Each new industrial revolution is exciting, and each cycle is subtly different from those that came before. The required study and reflection of what that means for investors today is complex, deserving a proper amount of time. As such this is not going to fit into a nice easy sound bite. In a world of high frequency trading and momentum investing, I suspect a lasting edge can maybe be found by those prepared to do the work. Let’s see.

Before we start, I want to be clear, I am an AI technology bull, excited about all it can do for humanity. But I am also a cautious investor who has seen movies like this before.

Many years, many cycles – much writing

Very long-standing readers of our work will know the four credit crunch pieces I wrote in 2007-2010. In these I outlined what I thought I saw coming and the potential consequences. Today when investing, I see macroeconomics akin to using wing mirrors when driving a car. I.e. we are mostly engaged in stock picking, but you need to keep an eye on the macro world around you. Sometimes more closely than others – 2007-2009 and COVID were two such example periods. This looks like another.

The other research piece I would reflect on is our work on Netflix. In it (page 7) we outlined our thinking on capital cycles, explaining that we thought the peak capital chasing subscribers had passed, so going forward Netflix would have greater pricing power. This is an example of the sort of cycles happening within industries all the time (another example today is EVs with much capital chasing market share).

AI is different – It’s a major capital cycle

What is happening with AI is similar, but different. Mostly this is due to the scale of both the opportunity and the capital that is chasing it. But it is also due to the breadth of the industrial/financial and political players that are impacted/attracted to it. Today is reminiscent of 1999/2000, a period we will discuss in more detail. My studying of that period is not from textbooks, but from being a transport specialist who became a telecom specialist in 1999 at Merrill Lynch. Additionally, I started my career in the summer of 1987, 10 weeks before the stock market crash.

Since those days I have read many books on bubbles and capital cycles to supplement my own experience, and all are referenced at the end. Does that make me an expert on these cycles and what sets them apart? Who knows. What is true is that I have spent a good part of my career reflecting on these issues.

The mistake ALL investors make in capital cycles

Upfront I observe a clear investing mistake I have seen repeated in all such cycles. This is the ingrained nature of both camps. The early bulls are emboldened by their success, so tend to stay bullish at all valuations. The early bears just see more reason to be cynical as prices rise. Looked at 10 years later both camps spend many years being wrong, ingrained in their view, and rarely thinking openly.

That is why maybe a roadmap could help because in such periods even the very best investors need one. I also hope it will help us when the next phase occurs. I have seen up close the ingrained views in past cycles. Indeed, I was a non-believer in TMT 1999, but way too early. That ingrained scepticism cost me dearly as I did not realise the opportunities being offered to me in c.2003-5 (e.g. Amazon and Google).

Learning from this, I have taken a more open-minded approach to AI. Like others I’m impressed by what the technology can do, but still keen to make sure I get a margin of safety on the companies I am investing in. The result has seen me buy shares in businesses I see as long-term beneficiaries when offered at good valuations. However, I’m not chasing anything new (read unproven from an ROIC perspective). For all my open mindedness, I’m an ‘investor’, not a ‘speculator.’

John Maynard Keynes described investing as “the activity of forecasting the prospective yield of assets over their whole life.” Speculation he described as “the activity of forecasting the psychology of the market.”

The capital cycle framework

AI is here to stay. On that hopefully all can agree. So how do we as investors navigate this new world in the coming years/decades.

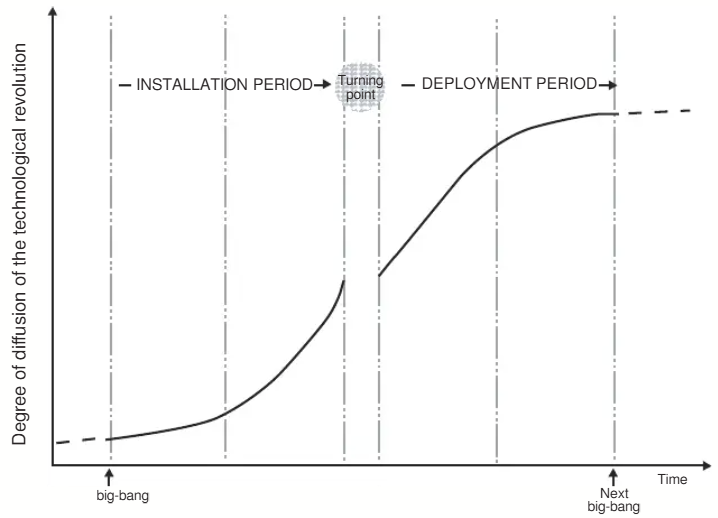

The most relevant of my study books to today’s starting point is Technological Revolutions and Financial Capital by Carlota Perez. Bearing in mind it was written in 2003 reading it today is like a handbook written for the here and now. A crucial number of conclusions it makes I have witnessed first-hand. The first of which is the separation between the Installation period of a new technology and the Deployment period of it.

In very broad terms, each (new technology) surge goes through two periods of a very different nature…. the first half can be termed the installation period.

It is the time when the new technologies irrupt in a maturing economy and advances like a bulldozer disrupting the established fabric and articulating new industrial networks, setting up new infra-structures and spreading new and superior ways of doing things.

At the beginning of that period, the revolution is a small fact and a big promise; at the end, the new paradigm is a significant force, having overcome the resistance of the old paradigm and being ready to serve as propeller of widespread growth.

The second half is the deployment period, when the fabric of the whole economy is rewoven and reshaped by the modernizing power of the triumphant paradigm, which then becomes normal best practice, enable the full unfolding of its wealth generating potential.

The turning point from Installation to Deployment is a crucial crossroads, usually a serious recession, involving a recomposition of the whole system… Source: Technological Revolutions and Financial Capital, Carlota Perez (emphasis ours)

Hopefully you see why this book is so useful to me. It is a literal textbook study of past cycles.

Fig.1: Anatomy of a capital cycle

Source: Technological Revolutions and Financial Capital, Carlota Perez

Source: Technological Revolutions and Financial Capital, Carlota Perez

Enter the Frenzy

The book then breaks down the Installation period into two separate sub-phases. These being ‘Irruption’ and ‘Frenzy.’

Most with a cool head today would surely conclude we are in the ‘Frenzy’ period. The question of course is how long this frenzy will last. This is particularly moot when we consider what normally happens next…

Towards the end of the installation period, there is a phase of frantic investment in the new industries and the infrastructure, stimulated by a stock market boom that usually becomes a bubble that inevitably collapses in one way or another. Source: Technological Revolutions and Financial Capital, Carlota Perez

As the book highlights what separates these Installation and Deployment phases is usually a stock market crash or recession. This is interesting and borne out by my TMT 1997-2004 experience.

I also suspect, such an event is not at the forefront of many investors’ minds right now! (Shiller Crash confidence index here). I note that the TMT/Dotcom stock market ‘Frenzy’ period lasted less than two years (mid-1998-March 2000). Below we will talk about the cult figures that define these periods and the roles they play. But here is Peter Thiel on PayPal’s need for capital.

“We knew we needed more funding. We also knew that the boom was going to end. On Feb 16, 2000 the Wall Street Journal ran a story lauding our growth and suggesting that PayPal was worth $500m. When we raised $100m the next month our lead investor took the journals back of the envelope valuation as authorative. That March 2000 funding bought us the time we needed to make PayPal a success. Just as we closed the deal the bubble popped.” Source: Peter Thiel, Zero to One 2014

The best founders/visionaries like Thiel know these up cycles don’t last, and to outcompete others they need to raise lots of capital while it’s cheap. With that in mind, don’t expect them to chat to you about the risks to the capital you are being asked to provide!! #eyeswideopen

Demand is the red herring (#Captial Returns)

It is worth us asking ourselves the following question. If the 1998 outlook for fibre/mobile demand was so high (and has ultimately proved correct) why did we see such aggressive collapses in Nasdaq/telecom share prices in the 2000-2003 period? The answer is not to be found in a study of demand, but through a study of supply. A new technological advancement starts with a few maverick inventors and ends with Wall Street throwing every bit of capital it can at the opportunity.

With all incentivised to raise capital (corp execs wanting scale to build rollouts faster than peers and bankers wanting fees) there is every reason to see upsides for new products and services far clearer than downsides. Simplistically if demand is thought to be 10x, but this rises to 150x everyone (CEOs, bankers, shareholders, press, politicians) is uber-excited. But capital chases this potential demand aggressively and no one is being too picky about things like risk adjusted returns on capital. As such when the dust settles maybe 300x of supply was built to chase 150x of demand. The result is ROICs collapse, the money dries up and the harder questions start being asked… to which few perma-bulls have any answers. This is a capital cycle. This is what happened in 1997-2000, and looks to be repeating itself in a fashion today.

‘In virtually all financial innovations and investment fads, Wall Street creates additional supply until it equals and then exceeds market demand. The profit motivation of Wall Street firms and the intense competition among them render any other outcome unlikely. Seth Klarman, Margin of Safety, 1991

Everyone drinking the same Kool-Aid

The other crucial thing to understand about such cycles is that they are circular. In theory companies and the owners of their shares, and press are totally separate, thinking independently and critically. In non-extreme periods this is true, but in a booming capital cycle it is not. Most companies are looking at the stock market/and their peers for what to do next. The stock market in turn watches the companies for their next move. And the press acts as a supercharger connecting to the two, as Thiel notes.

Senior CEOs and lead analysts achieve a cult like status, where investors hang on their every word. Their views (guesstimates of the future – they are nothing more) become somehow the firm building blocks of all forecasts. Today it is Jensen Huang and Elon Musk, but in 1998 in London it was Chris Gent and Hans Snook (in the US maybe Bernie Ebbers).

The projections that Gent/Snook made in c.1999 about the dominance of mobile were 100% correct (on a 30-year view) but that did not stop the Vodafone share price falling from 450p at its March 2000 peak to a trough of 115p two years later. The price it still trades at some 24 years later! (NB. Many young investors might not realise that Vodafone also broke the index funds. At one stage being c.12% of the UK stock market thus forcing passive buyers to over-own it). These are messages today’s investors need to heed. This is not about being bearish, or cynical on something that has gone up a lot or is valued highly. It is about asking honest questions of others, and yourself, on capital deployment. What is being spent today? What are the genuinely realistic ranges of return possible on that capital? Also, which companies can/cannot change course, if ROICs turn out worse than expected. I.e. which companies have bet the house on a certain outcome, and which could pivot and survive. My views on which companies are well and badly positioned today we will look at in the next piece.

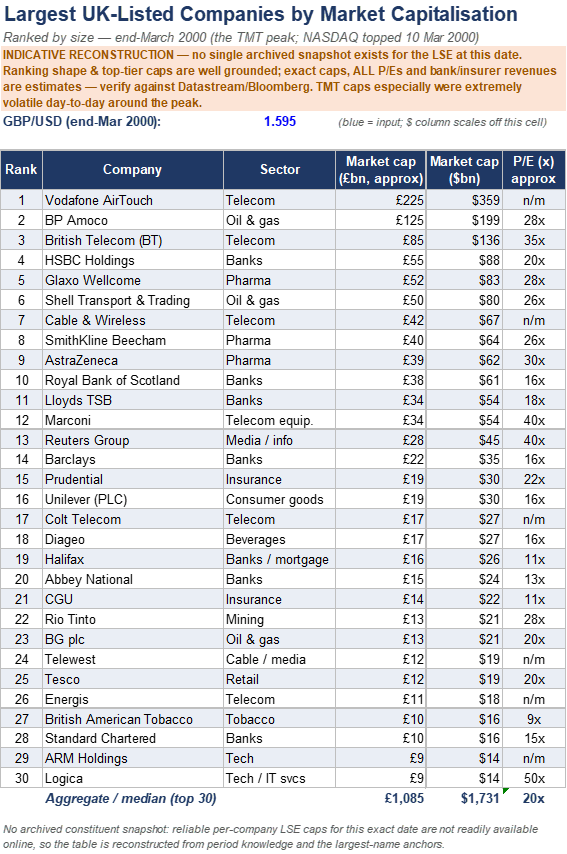

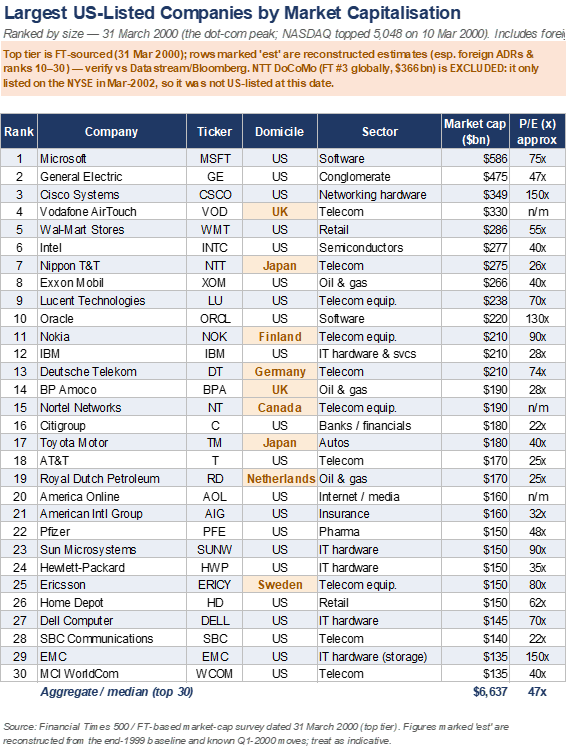

In the Appendices we show (helped by AI of course) the top 30 UK and US quoted companies as of March 2000. It’s an interesting reminder.

A word on career risk

When you visit your Wealth Manager, or they in turn question a Fund Manager they might invest with, ‘risk’ will be spliced, diced and debated in numerous different ways. There will be slides, factor risks and even colour codes! However, the biggest real risk to many portfolios, particularly at market extremes will never even be discussed. This is ‘career risk’.

It is often only felt subliminally, but it is very real and it plays a big part in providing the capital that fuels the later installation stage of capital cycles. It can also cost the end investor dearly.

Momentum, quarterly reporting and index inclusions are amongst the running pressures that force the hands of so many mainstream capital deployers who control $trillions. But peer pressure trumps them all. No single one of these later-cycle investors moves the needle alone, but collectively everyone does. Yet all are highly intelligent and consider themselves independent in thought (#ref Kool-Aid).

In 2016-20 we saw a huge weight of such capital allocated to pay up for ‘franchise businesses.’ Each decision to invest re-enforced by the resulting momentum that drove higher valuations proving their theories correct. Today’s consensus is to invest in AI or more index funds maybe? With active managers finding it hard to match indices, it is logical for allocators to deploy more to passive. This in turn will support new issuance, especially for companies with low free floats and fast index inclusion (e.g. SpaceX, Anthropic etc…).

“Men think in herds… they go mad in herds, while they only recover their senses, slowly one by one” Charles Mackay

In a corporate world, having an outlier result vs. your peers is dangerous. For a few months fine, even a few quarters. Try it for a few years and see if you keep your job – you won’t. When cycles are short or confined to market sub-sets (like Netflix) differing views can co-exist and are even welcomed by corporate overlords. When a super capital cycle like this one comes along, almost all are forced to jump aboard. Interestingly, only then does the consistency bias kick in.

Consistency Bias

Humans find it hard to hold two conflicting views at the same time. As such investors don’t say “this looks crazy, but I’ll put 10% of my client capital into it to cover myself.” They want to buy some of what is hot to fit in, so they get busy rationalising it. Then they invest and make a little money, and as a result become fanboys. These weak holders drive up valuations, but they also play a part when prices fall later on. Without conviction or valuation back stops they will sell when they are losing money. Others then follow. This is momentum investing 101. It’s just disguised as something else right now…. and on steroids!

The eventual market saturation of Wall Street fads coincides with a cooling of investor enthusiasm. When a particular sector is in vogue, success is a self-fulfilling prophecy. As buyers bid up prices, they help to justify their original enthusiasm. When prices peak and start to decline, however, the downward movement can also be self-fulfilling.’ Seth Klarman, Margin of Safety. 1991

FOMO is just the same thing at a retail level. The reason the career risk point is perhaps more crucial is that the people making such decisions are senior and control $trillions. They have power and influence, so when they succumb to the up cycle, its success is seen to be ‘proven’ and re-enforced.

Remember that the same career risk/consistency bias applies to the companies also. Both to those at the centre of the technology change and those at the fringes. Oracle doesn’t want to sit by and watch others get rich on datacentres/AI. They want a piece of the action. Whether or not that decision is correct depends on the longer term returns they make on the capital invested. As an outsider to the company, you will assume they have done the work to have confidence in the future returns this will generate. They believe they have, but the assumptions behind their work might look a lot less believable 5 years on.

“There is nothing worse than watching your neighbour get rich” Charlie Munger

Dare you be a non-believer?

This heady cocktail of brilliant invention, imagination of its true potential, inspirational messiahs, and limitless capital creates a truly powerful, once in a lifetime draw. So powerful that few can resist the get-rich-quick mantra. The few that do are often older, so think they know better, or ‘too old’ to see how things can genuinely change. Either way the oversight brake a c.55-70y CIO might have had on a younger investment team is loosened. He is either so out of touch, as to get fired, or just keeps his head down. Other non-believers are treated like they are in Life of Brian. The result is that the young, and recently right, are mostly the voices we hear.

When the ducks quack feed ‘em

As an investor it always helps to know who you are buying from and why. Much analysis of this is done in secondary market investing. But in the Frenzy phase of a capital cycle this is more important than ever, yet it gets overlooked. Technology businesses by their very nature are loss making in their early years, earning their money (and value) further out. To make successful long-term outcomes more likely they need capital and they know it. The more competitive an industry is, the more they need (to outgun/outlast a competitor when building scale). Needless to say, if the industry is capital intensive the scale of capital required leaps further still. Oh, and in the same way investors want to buy shares when they are cheap, companies want to raise capital when it’s cheap too. That means they want high share prices and lots of capital raised at those prices. With all that in mind, don’t be expecting capital-raising CEOs to be giving you a balanced view of the future.

In that context Google’s recent equity raise stands out. This is not a company that looked like it needed equity. But with SpaceX raising $75bn, they did not want to be outgunned. So, taking a 2% dilution to get access to $85bn in equity is a logical step by a company trying to ensure its long-term dominance. Their rationale for them wanting to raise capital, and your decision to invest, however, need to be very different.

‘If you’ve been playing poker for half an hour and you still don’t know who the patsy is, it’s you!’ Warren Buffett

Setting the scene + Thanks

I hope this piece sets the scene for the framework I see when considering capital cycles. There is a great deal we can learn from the past. When something technologically new and significant happens there is an assumption by those at the sharp end that they are ground-breaking, therefore the old rules no longer apply. In technical matters this is likely true, but in the wave of capital allocation that follows and its consequences, it is not. Technological know-how might start the installation period of the cycle, but capital supply then amplifies it to epic proportions (the Frenzy).

When I decided to write this piece, I got in touch with a friend. Long since retired, he was a Senior TMT analyst throughout the whole of the 1995-2002 period. His role meant he was one of the cult-like figures of the time I refer to above. He also had amazing access to the senior company execs. His reflections helped me a great deal with some of what is above. In addition, he made a couple of other observations I think worth highlighting separately:

“If companies could get the capital, they invested. Availability of capital was key”

“In truth no one had any idea how big demand would be. What I have learnt is that you just cannot know the future”

“The CEOs were like gods, feted everywhere they went”

“It was hard to see a reason to be bearish”

“No single event marked the top, but the huge scale of M&A was the warning sign”.

Thank you ex-Analyst X for your time, reflections and friendship.

Signing off

In Part 2 we will look at how we might navigate the world as it is today, in 2026. Observing lessons from the past is easy with a little study. Working out how to apply them in the future will be more challenging! Let’s leave the last words to my new favourite author, Carlota Perez.

The full fruits of the technological revolutions that occur about every half century are only widely reaped with a time-lag.

Historically, those decades have brought the greatest excitement in financial markets, where brilliant successes and innovation share the stage with great manias and outrageous swindles. They have also ended with the most virulent crashes, recessions and depressions, later to give way, to a period of widespread prosperity, based on the potential of that particular set of technologies.

Financial capital plays a crucial role all along. It first supports the development of the technological revolution, it then contributes to deepen the mis-match leading to a possible crash, it later becomes a contributing agent in the deployment process once the match is achieved. Source: Technological Revolutions and Financial Capital, Carlota Perez

See you in Part 2!

Kind regards

Andrew + Team

Book sources:

The Hour Between Dog and Wolf, John Coates

Mastering the Market Cycle, Howard Marks

Capital Returns, Edward Chancellor

Capital Account, Edward Chancellor

Devil Take the Hindmost, Edward Chancellor

Extraordinary Popular Delusions and the Madness of Crowds, Charles Mackay

The Directors and employees of Holland Advisors may have a beneficial interest in some of the companies mentioned in this report via holdings in a fund that they also act as managers to.

Appendix

Fig.2: Largest UK companies by market cap, March 2000

Fig.3: Largest US companies by market cap, March 2000

Disclaimer

This document does not consist of investment research as it has not been prepared in accordance with UK legal requirements designed to promote the independence of investment research. Therefore even if it contains a research recommendation it should be treated as a marketing communication and as such will be fair, clear and not misleading in line with Financial Conduct Authority rules. Holland Advisors is authorised and regulated by the Financial Conduct Authority. This presentation is intended for institutional investors and high net worth experienced investors who understand the risks involved with the investment being promoted within this document. This communication should not be distributed to anyone other than the intended recipients and should not be relied upon by retail clients (as defined by Financial Conduct Authority). This communication is being supplied to you solely for your information and may not be reproduced, re-distributed or passed to any other person or published in whole or in part for any purpose. This communication is provided for information purposes only and should not be regarded as an offer or solicitation to buy or sell any security or other financial instrument. Any opinions cited in this communication are subject to change without notice. This communication is not a personal recommendation to you. Holland Advisors takes all reasonable care to ensure that the information is accurate and complete; however no warranty, representation, or undertaking is given that it is free from inaccuracies or omissions. This communication is based on and contains current public information, data, opinions, estimates and projections obtained from sources we believe to be reliable. Past performance is not necessarily a guide to future performance. The content of this communication may have been disclosed to the issuer(s) prior to dissemination in order to verify its factual accuracy. Investments in general involve some degree of risk therefore Prospective Investors should be aware that the value of any investment may rise and fall and you may get back less than you invested. Value and income may be adversely affected by exchange rates, interest rates and other factors. The investment discussed in this communication may not be eligible for sale in some states or countries and may not be suitable for all investors. If you are unsure about the suitability of this investment given your financial objectives, resources and risk appetite, please contact your financial advisor before taking any further action. This document is for informational purposes only and should not be regarded as an offer or solicitation to buy the securities or other instruments mentioned in it. Holland Advisors and/or its officers, directors and employees may have or take positions in securities or derivatives mentioned in this document (or in any related investment) and may from time to time dispose of any such securities (or instrument). Holland Advisors manage conflicts of interest in regard to this communication internally via their compliance procedures.